TAMPA FL FHA MORTGAGE LENDERS

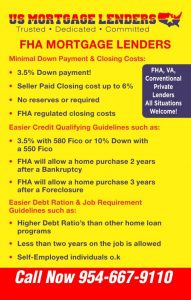

TAMPA FLORIDA FHA MORTGAGE LENDERS HAVE MINIMAL DOWNPAYMENT AND CLOSING FEES:

- Down payment only 3.5%of the purchase price.

- Gifts from family or Grants for down payment assistance and closing costs OK!

- Seller can credit buyers up to 6%of sales price towards buyers costs.

- No reserves or future payments in account required.

- FHA regulated closing costs.

TAMPA FLORIDA FHA MORTGAGE LOANS ARE EASY TO QUALIFY FOR BECAUSE YOU CAN:

- Purchase a Florida home 12 months after a chapter 13 Bankruptcy

- Purchase a Florida 24 months after a chapter 7 Bankruptcy.

- FHA will allow a FHA mortgage 3 years after a Foreclosure.

- Minimum FICO credit score of 580 required for 96.5% financing.

- Bad credit Florida FHA mortgage approvals minimum FICO credit score of 530 required for 90 FHA financing.

- No Credit Score Florida mortgage loans & No Trade Line Florida FHA home loans.

TAMPA FLORIDA FHA MORTGAGE LOANS ALLOW HIGHER DEBT TO INCOME & EASIER JOB QUALIFYING

- FHA allows higher debt ratio’s than any other Florida home loan programs.

- Less than two years on the same job is OK!

- Self-employed buyers can also qualify for FHA.

- Check Florida FHA Mortgage Articles for more information.

TAMPA FLORIDA FHA MORTGAGE BULLETS:

-

TAMPA FHA MORTGAGE LOANS ARE EASY TO QUALIFY & EASY TO AFFORD-

The Federal Housing Administration (FHA) insures FHA mortgage loans against default as a way to help first-time home buyers, as well as lower and middle-income citizens. Unlike traditional mortgages, FHA loans require lower down payments and easier credit requirements to secure a loan. In fact, FHA mortgages now make up nearly a third of all new purchase mortgages in America. Get Started Now!

-

TAMPA FLORIDA BAD CREDIT FHA MORTGAGE LENDERS?

-That is Not a Problem- Florida Mortgage Lenders.com is ready to help all Florida residents in all saturation with their next Florida home purchase! Whether you’re looking for a turn-key property, hoping to refinance your current Florida home, or purchase a fixer-upper, Florida Mortgage Lenders.com can help you secure an FHA mortgage loan in the in every city and county in Florida. With an FHA mortgage loan, you can buy a property with little money down, or cash out using equity in your current home. Don’t hesitate – give us a call today to find the right FHA mortgage programs for your situation. Ready to apply now? Click the button at the bottom of the page. Our Florida specialists look forward to helping you secure your new home!

-

TAMPA FLORIDA FIRST TIME HOME BUYERS-

For the last 10 years, Florida Mortgage Lenders.com has served Florida as one of the top Florida FHA Mortgage Lenders. We’ve helped residents secure Florida FHA loans in every city and county in Florida. Buying or refinancing a home can be tricky, but we are here to help. Imagine a streamlined, stress-free Florida mortgage approval process: that’s what you get when you apply for a mortgage with us! We take pride in taking care of our clients for life.

-

TAMPA FLORIDA FHA MORTGAGE REQUIREMENTS AND BENEFITS-

Florida FHA Mortgages are only available for a borrower’s Primary Residence. You cannot

-

TAMPA FHA MORTGAGE FOR HOME BUYERS

The fact is, there are a wide range of FHA home loans available to qualified Florida mortgage applicants. And the real truth is, these programs are based on a common sense approach to lending and approval is not heavily based on your credit score. Many people find this very difficult to believe, but it is in fact dictated by HUD guidelines that credit scores cannot be considered during underwriting, only credit quality instead. This gives consumers who might not otherwise have the ability to secure a low fixed interest rate mortgage ample opportunity to qualify. It is one of the biggest benefits that many FHA mortgage loans offer to people just like you.

-

TAMPA FLORIDA FHA STREAMLINE REFINANCE

– With the FHA streamline mortgage program, so long as your mortgage payments have been on time for the prior 12 months, you can inexpensively take advantage of any improvements in market interest Rates. Even if you had a “payment” bump in the road, you can still possibly qualify for a FHA streamline mortgage refinance with the right circumstances!

-

ABOUT FLORIDA-MORTGAGE-LENDERS.COM

has no affiliation with the government, including HUD or the FHA. In addition, our program is not pre-approved by the government or your lender. Your lender may not necessarily change your loan based on your acceptance of our offers.

-

TAMPA FLORIDA HOMEBUYERS APPLY FOR A FLORIDA FHA MORTGAGE NOW!!

Florida Mortgage requirements are always changing, and Florida homebuyers can count on Florida Mortgage Lenders.com to provide up-to-date information support. In addition, we are one of Florida most active and experienced Florida mortgage lenders. With so many options out there, our job is to help you make the best decision for you. We make the FHA application process easy to understand and are always here to answer questions. Our website is also packed with information for you to browse. Our secure mortgage application is available online when you’re ready to apply for a mortgage and we will even call you to start the process.

3.5% TAMPA FLORIDA FHA MORTGAGE LENDERS – TAMPA FL FHA MORTGAGE LENDERS —HILLSBOROUGH COUNTY FLORIDA FHA MORTGAGE LENDERS – TAMPA FLORIDA FHA MORTGAGE LENDERS — TAMPA FL FHA MORTGAGE LENDERS

CATEGORY: FHA MORTGAGE GUIDELINES

How to Get An FHA Mortgage Lenders Approval With Bad Credit?

The bad credit FHA mortgage lenders must use a traditional credit report, if available. A Residential Mortgage Credit report (RMCR) must be obtained from an independent credit reporting agency. The Bad credit FHA mortgage lenders must use the same credit report and credit scores sent to TOTAL Mortgage Scorecard. If a traditional credit report is not…

Why Are FHA Mortgage Lenders So Popular With For Homebuyers?

FHA mortgages lenders offer many advantages and protections that only come with an FHA mortgage: Lower Down Payment: FHA loans have a low 3.5% down payment and that money can come from a family member, employer or charitable organization as a gift. Conventional mortgage lenders do not allow this. Easier to Qualify: Due to the…

Do FHA Mortgage Lenders allow Flipping?

Property Flipping is indicative of a practice whereby recently acquired property is resold for a considerable profit with an artificially inflated value. The term Property Flipping refers to the purchase and subsequent resale of a property in a short period of time. The eligibility of a property for an FHA mortgage lender is determined by…

Do FHA Mortgage Lenders Allow Collections or Judgements?

COLLECTIONS-JUDGEMENTS COLLECTIONS- FHA Mortgage applicants are not required to pay off all collection accounts. However, outstanding collections will reflect on your creditworthiness overall and may be held against you. In this case, one or more of the collections may need to be paid off in order to improve your credit score and show your willingness to pay debts….

Do FHA Mortgage Lenders Lend on Condos?

Yes, FHA mortgage lenders will finance FHA Approved Condominium under the 203b program, FHA mortgage lenders provide insurance on FHA mortgage loans secured by one-family condominium Units located in FHA-Approved Condominium Projects and in Units located in Condominium Projects not approved by FHA. FHA Mortgage loans are made by FHA-approved mortgage lenders, such as…

Will FHA Mortgage Lenders Accept bad credit? What are the requirements for a manually underwritten mortgage?

Will FHA Mortgage Lenders Accept bad credit? What are the requirements for a manually underwritten mortgage? The bad credit FHA mortgage lenders must use a traditional credit report, if available. A Residential Mortgage Credit report (RMCR) must be obtained from an independent credit reporting agency. The Bad credit FHA mortgage lenders must use the same…

Can I use FHA Mortgage Lenders to buy a Second Home?

Secondary home refers to a dwelling that an FHA mortgage applicant occupies, in addition to their principal home, but less than a majority of the calendar year. A Secondary home does not include a vacation home. Secondary homes are only permitted with written approval from the FHA mortgage lenders approved jurisdictional Homeownership Center provided that: …

Do FHA Mortgage Lenders Require Collections To Be Paid Off To Qualify For An FHA Mortgage?

A Collection Account refers to a FHA mortgage applicants loan or debt that has been submitted to a collection agency by a creditor. If the credit reports used in the analysis show cumulative outstanding collection account balances of $2,000 or greater, the FHA mortgage lender must: • verify that the debt is paid in full…

Do FHA Mortgage Lenders require reserves for manually underwritten loans?

Yes, the Mortgagee must verify and document Reserves equivalent to (1) one month’s Principal, Interest, Taxes, and Insurance (PITI) after closing for one- to two-unit Properties. The Mortgagee must verify and document Reserves equivalent to (3) three months’ PITI after closing for three- to four-unit properties. What are FHA mortgage reserves? FHA Mortgage reserves are…

Do FHA Mortgage Lenders Allow Gift of Down payment To come from Friends or Employer?

Do FHA Mortgage Lenders Allow Gift of Down payment To come from Friends? FHA mortgage lenders refer to gifts or contributions of cash or equity with no expectation of repayment. Gifts may be provided by: • a close friend with a clearly defined and documented interest in the Borrower; • the Borrower’s Family Member; •…

Do FHA Mortgage Lenders allow employers gift the borrower’s down payment?

Do FHA Mortgage Lenders allow employers gift the FHA mortgage applicants down payment? Employer Assistance refers to benefits provided by an employer to relocate the FHA mortgage applicants or assist in the FHA mortgage applicants housing purchase, including closing costs, Mortgage Insurance Premiums (MIP), or any portion of the FHA mortgage applicants Minimum Required…

Do FHA mortgage Lenders allow realtors to give a gift of their commission for the down payment?

Do FHA mortgage Lenders allow realtors to give a gift of their commission for the down payment? Can A Realtors real estate Commission from Sale of Subject Property refers to the Borrower’s down payment portion of a real estate commission earned from the sale of the property being purchased. FHA mortgage lenders may consider Real…

FHA Mortgage Lenders Jacksonville Florida

JACKSONVILLE FL FHA MORTGAGE LENDERS 3.5% Lowest Down payment Option! Home Sellers are allowed to pay up to 6% of your closing costs. Higher debt-to-income ratios allowed up to 56%. Down payment can be a gift from a family member. FHA Mortgage insurance is required for the life of the loan. Non-occupying FHA co-borrowers are…

Do FHA Mortgage Lenders Allow Gifts for Down Payment And Closing Cost?

Do FHA Mortgage Lenders Allow Gifts for Down Payment And Closing Cost? FHA Mortgage Lenders refer to Gifts as contributions of cash or equity with no expectation of repayment. FHA Mortgage Lenders Allow Gift Funds from the following approved sources • The FHA mortgage applicants Family Member; • The FHA mortgage applicants employer or labor…

Will FHA Mortgage Lenders Allow More Than 1 FHA Mortgage?

FHA mortgage lenders will not insure more than one Property as a Principal Residence for any FHA mortgage applicants, except as noted below. FHA mortgage lenders will not insure a Mortgage if it is determined that the transaction was designed to use FHA mortgage insurance as a vehicle for obtaining Investment Properties, even if the…

FHA Mortgage Lenders Cash Out and Rate Term Refinance

FHA Mortgage Lenders Rate Term Refinance Properties owned > 12 months: The subject property must be owner occupied for at least 12 months at the time of case number assignment. Properties owned < 12 months: The subject property must be owner occupied for the entire period of ownership at the time of case number assignment. …

FHA Mortgage Lenders Compensating Factors

FHA COMPENSATING FACTORS What are FHA compensating factors? (FHA compensating factors are the stronger elements of a credit application that it offsets something weaker in the application) but it’s more complicated than that. Different FHA Lenders manage the consideration of compensating factors in different ways. FHA’s written guidelines outline specific examples of what FHA compensating factors…

FHA Mortgage Lenders Manual Underwriting Approvals

FHA Manual Underwrite Lenders Specifications CREDIT SCORE RANGE MAXIMUM QUALIFYING RATIOS APPLICABLE GUIDELINE 500 – 579 ·31/43 ·Energy Efficient Homes may stretch ratios to 33/45 ·Max LTV 90% unless cash out (80%) ·No gifts ·No down payment assistance ·No streamlines ·One month in reserves for 1-2-unit Properties, three months in reserves for 3-4-unit properties (cannot be a…

FHA Mortgage Lenders Allow Non Occupant Co Borrowers

FHA Mortgage Lenders Non-Occupant co borrower 1-Unit properties only. Max mortgage is limited to 75% LTV unless non-occupying co- borrower’s meet FHA definition of ‘family member’. Seller cannot be non-occupant co-borrower. Non-occupant co-borrowers may be added to improve ratios. Non-occupant co-borrowers cannot be used to overcome or offset borrower’s derogatory credit. The non-occupying borrower arrangement…

FHA Mortgage Lenders Source Of Down Payment And Reserves

FHA Mortgage Lenders require a minimum cash investment from FHA mortgage applicants own funds and/or gift (no cash on hand allowed when FHA mortgage applicants uses traditional banking sources and has traditional credit history). Any deposit 1 % and greater of the sales price must be sourced and seasoned. An aggregate of deposits 1 °/o…

FHA Mortgage Lenders Can Use Non Taxable Income To Qualify

FHA Mortgage Lenders Allow Nontaxable income such as Social Security, Pension, Workers Comp and Disability Retirement income can be grossed up 115% of the income can be used to qualify for an FHA mortgage loan. Unacceptable Sources of Income Include: The following income sources are not acceptable for purposes of qualifying the borrower: Any unverified…

What Are FHA Mortgage Lenders Debt To Income Ratio Requirements?

Debt Ratio – Loans with AUS Approve/Eligible – follow AUS decision. Credit scores of 640 and under and DTI greater than 43% regardless of AUS decision require explanation for derogatory credit and a VOR or rent free letter (if applicable). Manually underwritten loans with FICO score> 580 may exceed 31°/o/43°/o ratios with acceptable compensating factors…

FHA Mortgage Lenders Cash-Out Refinance Payment History

FHA Mortgage Lenders Mortgage/Rental History Payment History All Cash Out Refinance Transactions and Manually Underwritten Rate Term Refinance Transactions: No 30 Day late payments within the last 12 months of case number assignment. FHA Mortgage Lenders Rate and Term Refinance Transactions: AUS Accept – follow AUS. ALSO CHECK FHA Mortgage Lenders Compensating Factors FHA COMPENSATING…

FHA Mortgage Lenders Minimum Trade Line Requirement

FHA Minimum Tradelines or Minimum Credit Reporting History FHA mortgage applicants must have sufficient credit history to generate a valid FICO score, or FHA mortgage applicants must meet the non-traditional FHA mortgage lenders guidelines listed below. Generally, an acceptable credit history does not have late housing, installment debt or major derogatory revolving payments. Authorized tradelines…

How Do FHA Mortgage Lenders calculate student loan payments?

How Do FHA Mortgage Lenders treat Student Loans? Student Loan Payments – Student loan(s) would be calculated as follows, regardless of the payment status. FHA mortgage lenders must use either the greater of: 1% of the outstanding balance on the loan; or the monthly payment reported on the FHA mortgage applicants credit report; or the…

FHA Mortgage Lenders Approval With Disputed Accounts

FHA Mortgage Lenders Approval With Disputed Accounts derogatory accounts >= $1,000 cumulative must be downgraded to “Refer” manual underwrite. Medical and accounts resulting from identity and credit card theft or unauthorized use are excluded. A letter from the creditor, police report, etc. is required. Disputed non-derogatory accounts are excluded from the $1000 cumulative total which…

FHA Mortgage Lenders Approval With Loan Modifications

FHA Mortgage Lenders Approval After A Loan Modifications FHA Mortgage Lenders Automated Underwriting System required to follow guidance for acceptable mortgage history. Manual Underwrite -follow manual mortgage requirements (Ox30 for most recent 12 months and 2×30 for the most recent 24 months on the modified mortgage.) Payment history is evaluated based upon the FHA mortgage…

FHA Mortgage Lenders Qualifying Requirements After A Short Sale

FHA Mortgage Qualifying After A Short Sale Any Short Sale within three (3) years of the case assignment requires a manual underwrite. An FHA mortgage applicant who is in default at the time of short sale/restructure or pre-foreclosure or late on any mortgage or installment obligations within 12 months of the short sale is not…

FHA Mortgage Lenders After Foreclosure or Deed In Lieu of Foreclosure

What are the guidelines for FHA mortgage applicants with a previous foreclosure or deed-in-lieu of foreclosure? A FHA mortgage applicants is generally NOT eligible for a new FHA-insured mortgage if the Borrower had a foreclosure or a deed-in-lieu of foreclosure in the last 3 three-year period prior to the date of case number assignment. This…