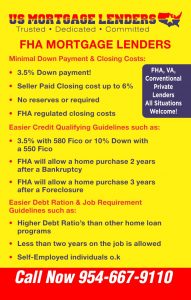

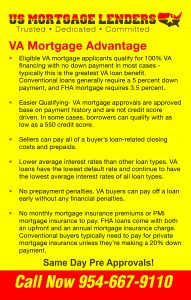

FHA/VA MORTGAGE PROGRAMS – 3.5% Down with a 580 fico. 100% VA financing with a 580 fico. FHA/VA Manual Approvals when your bank says NO! We say Yes! Purchase 3 years after Foreclosure, 2 years after a Chapter 7 Bankruptcy. 12 months after a Chapter 13 bankruptcy.

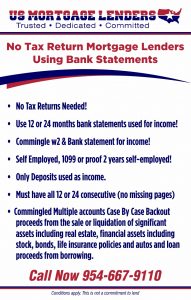

ONE-YEAR INCOME VERIFICATION – Qualify income with just 1 year of recent W2 + YTD paystub OR self-employed 1-year tax return. Max LTV 80%.

RECENT CREDIT EVENT – Recent Foreclosure, Bankruptcy, and Short Sale allowed. Mortgage rates ok. Min FICO 500 with compensating factors and good payment history.

INVESTOR NO RATIO – No income verification or debt service coverage. 75% max LTV for purchase and rate & term refinance, 70% LTV for cash out.

INVESTOR DEBT SERVICE COVERAGE – Subject property market rent covers proposed PITI to qualify. 80% LTV allowed for purchase AND rate & term. 90-day seasoning on cash out.

ASSET DEPLETION – Assets to qualify. 100% of retirement accounts can be used. The percentage of equity in real estate owned can also be used in calculations. Max DTI is 59%.

FOREIGN NATIONAL – No Ratio, Debt Service Coverage, and 1-year income verification ALLOWED. Rates as low as 5.625%.

| Do you have less than perfect credit? Or have less than 20% for a down? Then the FHA or VA mortgage might be right for you. And if not, we have other Options for you! |

Good Credit –Bad Credit – No Credit+ No Problem + We work with everyone towards home ownership! Whether you’re a first time home buyer, moving to a new home, or want to FHA refinance your existing conventional or FHA mortgage, we will show you how to purchase or refinance a home using our stated mortgage program or bank statement only mortgage program.

When you decide to apply for a FHA home loan throughFHA mortgage lender you need to know you’re dealing with experienced full-time mortgage lending professionals who know FL real estate. We offer a huge assortment of FL VA lendersincluding FHA, Conventional& Private mortgage programs built around Florida and Georgia home buyers and homeowners.

Whether you’re buying a first home using our greatFHAmortgage program or refinancing a home you already own using traditional Florida mortgage financing, nothing helps more than having a seasoned Florida FHA mortgage lenderworking hard answer all your FloridaFHA mortgage questions!

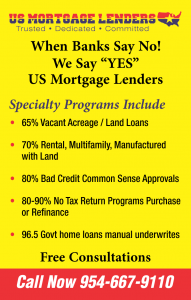

FHA MINIMAL DOWN PAYMENT AND FEES:

- Down payment only 3.5% of the purchase price, down payment assistance and closing costs OK!

- Sellers can credit the buyer’s up to 6% of sales price towards buyers costs and pre-paid.

- No reserves or future payments in account required.

- FHA regulated closing costs.

- Read more about buying a home with an FHA mortgage Bad Credit –No Credit – FHA Guidelines –Debt To Income Limits –

FHA IS EASIER TO QUALIFY:

- 12 months after a chapter 13 Bankruptcy FHA mortgage Lender approvals!

- 24 months after a chapter 7Bankruptcy FHA mortgage Lender approvals!

- 3 years after a Foreclosure FHA mortgage Lender approvals!

- No Credit Score FHA mortgage Lender approvals!

- 580 required for 96.5% financing or 3.5% down payment FHA mortgage Lender approvals.

- 500 required for 90% financing or 10% down payment FHA mortgage Lender approvals.

- Bad Credit with minimum 500 FICO credit score with 10% Down Payment FHA.

FHA OK WITH HIGHER DEBT EASIER QUALIFYING:

- FHA allows higher debt ratio’s than any conventional mortgage loan programs.

- Less than (2) two years on the same job is OK!

- Self-employed buyers can also qualify with FHA Mortgage Lenders.

- Read More about Gifts For Down Payment – Documents Checklist – Debt To Income – Student Loans.

| Regardless of your situation, we work with EVERYONE to get them Pre Approved! We willcounsel you FREE OF CHARGE until you qualify for a mortgage! |

FHA MORTGAGE ALL PROPERTY TYPES:

- Single-family Homes

- Town House- check for lot and/or block legal descriptions.

- Villas- check for lot and/or block legal descriptions.

- Modular Homes

- FHA Approved condominium – Search Florida FHA Approved Condos

FHA MORTGAGE BENEFITS: The FHA mortgage is so popular is because Florida mortgage applicants use them are able to take advantage of benefits and protections unavailable with any other mortgage loan program. Loans through the FHA are insured by the government, so the Florida mortgage lenders that approve these loans are more lenient. The advantages outweigh any other mortgage program and include and include the following:

- Lower Cost & Fees- In addition to lower interest rates, FHA borrowers enjoy lower costs on other fees like closing costs, FHA mortgage insurance and govt regulated closing cost.

- Easier to Qualify- While most mortgage loans prohibit applicants with bad credit history and low credit scores, the FHA mortgage loans available with lower requirements so its easier for you to qualify.

- Lowest Interest Rates- You’ve heard the horror stories of subprime borrowers who couldn’t keep up with their mortgage interest rates. Well, FHA loans usually offer lower interest rates to help homeowners afford housing payments.

- Bankruptcy / Foreclosure- Even If you’ve filed for bankruptcy or suffered a foreclosure in the past few years doesn’t mean you’re excluded from qualifying for an FHA loan. As long as you meet other requirements that satisfy the FHA, such as re-establishment of good credit, solid payment history, etc., you can still qualify.

- No Credit Score/ No Trade Lines OK! – The FHA usually requires two lines of credit for qualifying applicants. If you don’t have a sufficient credit history, you can try to qualify through a substitute form.

For many Florida FHA mortgage applicants, using an FHA mortgage can really make the difference between owning your dream house affordability and getting out of the never ending rental trap. The FHA mortgage provides a wealth of benefits for Florida mortgage applicants that qualify, so please make full use of them.

FHA BUYER QUESTIONS:

- What is an FHA Mortgage loan? The FHA is a division of the Department of (HUD) Housing and Urban Development. An FHA mortgage loan is a mortgage that is insured by the Federal Housing Administration (FHA) and funded by private Florida FHA approved mortgage lenders.

- Are FHA mortgage for first time home buyers only?NO, FHA mortgage loans are NOTfor first–time buyers only. FHA loans can be used by first-time buyers and repeat buyers alike. The FHA mortgage is often marketed as a product for “first–time buyers” because of its low down payment and flexible qualifying requirements. FHA mortgage applicants can purchase anFHA approved investment property using and FHA mortgage loan.

- How Does The FHA Mortgage Insurance Work? Anyone who takes out FHA mortgage finances the mortgage insurance into the loan amount. This “Up Front Mortgage Insurance ” cost is called the “UFMIP”. The upfront mortgage insurance premium paid on all FHA mortgages is paid to the government and use the funding fee money to reimburse Florida FHA Mortgage lenderswho were forced to foreclose on mortgages that were financed tobad credit mortgage applicants. Think of the funding fee as the foreclosure “insurance fund” for the FHA Florida Mortgage Lenders. In addition to the upfront funding fee, the borrower is also required to pay a small monthly fee to the FHA as part of their monthly mortgage payment. The monthly fee is called monthly MIP or mortgage insurance premium.

- Do I have to be a first-time mortgage buyer to use the FHA mortgage? No you do not have to be a first time Florida home buyer but the FHA mortgage is only for a Primary home purchase only.

- Can I roll all the closing costs into the FHA mortgage? You are permitted to finance the upfront FHA funding fee only.FHA mortgage closing costs can be paid by the seller up to 6% and must be negotiated up front in your purchase and sale agreement.

- Can I get an FHA Mortgage after a Foreclosure or Bankruptcy? YES! you can qualify for an FHA mortgage 3 years after the title was transferred out of your name.A borrower may also still qualify for an FHA insured loan after declaring Chapter 13 bankruptcy, if at least 1 year of the bankruptcy payout period has passed and the borrower has been making satisfactory payments. In these cases, the FHA mortgage applicant must also request permission from the court to enter into a new FHA mortgage loan. declaring Chapter 7 bankruptcy, if at least 2 years have passed since the bankruptcy discharge date. FHA mortgage applicants must also have re-established good credit or have opted to incur no new debts (this means you specifically chose to take out no new loans, credit cards, etc.)

- What is the minimum down payment for FHA Mortgage? Currently, 3.5% can from family gift or grant.

- Can my parents or other relatives give me money? Yes, provided the money is considered a gift and your relative sign and date the proper gift letter documentation.

- Is there a maximum FHA Mortgage Loan Amount? Yes, see maximum loan limits below based on the Florida county.

FHA MORTGAGE LINKS OF INTEREST:

We provide free credit counseling to and work with everyone to get PRE APPROVED!