CondoTel Florida Mortgage Lenders

Florida Condotel No Doc And Alt Docs Mortgage Programs Links Below

- No Tax Return Florida Condotel Mortgage Lenders

- Bank Statement Florida Condotel Mortgage Lenders

- Stated Income Florida Condotel Mortgage Lenders

DSCR Florida Condotel Mortgage Lenders – Use Condotel Rental Income To Qualify!

ALL INFORMATION IS NOT TO BE RELIED ON CALL US FOR UP-TO-DATE TERMS AND CONDITIONS

Condotel Mortgage Lenders Borrowers Profile Include:

US citizens, Perm Resident Aliens, and Non-Perm Resident Aliens. LLC w/ pers. guarantee.

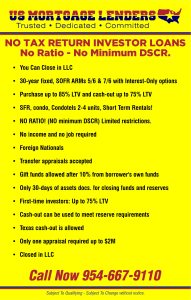

Debt Service Coverage Ratio (DSCR) = Rental Income divided by PITIA. Short-term rental income max LTV 65% Short-term rental income requires Senior Management approval. Minimum DSCR 1.0X, below 1.0X requires Senior Management approval

Rental Income Verification

= Lower of Gross Rent lease or Form 1007 Purchase: Market rents FNMA form 1007 for SFR

Refinance: Market rents or lease with canceled checks for 2 months

Experience Review– First-time investor must own primary residence for 12 months. Max LTV 80%

Reserve Requirements – 3 months PITI. No reserves required < 65% LTV for purchase transactions Cash Out may count towards reserves

Occupancy

Non-Owner Occupied. Certification of intent not to occupy is required. Property cannot be rented to a family member

Cash Out

Maximum $500,000. Must be used for business purpose. Minimum FICO 700 for cash out.

Must have owned the property prior for 6 months. Max 65% LTV for condotel and requires Senior Manager approval

Loan Sizes--$1,500,000 Max (Minimum $150,000)

Min FICO 680

Can also qualify w/start rate on I/O pmt

Not permitted on a Texas (a)(6)/primary cash-out

Mortgage Delinquency History–0x30x24

Credit Event Seasoning – BK, FC, SS, Mod: 36 months

Asset Verification

Sourced and Seasoned 60 days. Gift Funds at Mgt Discretion.

Prepayment Penalty

5% on any amount prepaid for 3 year term

Loan Terms

30-Year Amortized & Term – 5/1 Hybrid ARM or 30-Yr Fixed

Request to waive impounds on loans < 75% LTV, Min FICO 680 only with Senior Manager approval

All loans in flood zone require impounds for T&I

Credit History

Min Tradelines: 4 tradelines, at least 2 active

Tradeline History: 2 years

Property Types: Condotel

No Texas properties > 10 Acres for cash-out refi

Condotels: Purchase, > 680 FICO, R/T & C/O > 740 FICO. All C/O on condotels requires senior mgt approval For 5-8 Units –

Deviations For Condotel mortgage lenders is case by case with compensating factors

WHAT ARE FLORIDA Condotel ‘S AND HOW DO THEY WORK?

Florida Condotel is like a Condotel minium project that is operated as a Florida hotel with a registration desk, cleaning service and more amenities along with rental options. These Condotel units are individually owned. The biggest difference is that Condotel unit owners also have the option to place their units in the Florida Condotel -hotel’s rental program where it is rented out and managed by Condotel management like any other hotel room.

Condotel -MORTGAGE LENDER’S TYPES ON OF FINANCING

- 1 – 4 Unit Residential Properties

- Acreage, Hobby Farm & Unique Property

- Warrantable Florida Condotel Mortgage Lenders

- Non-Warrantable Florida Condotel Mortgage Lenders

- Condotel Florida Mortgage Lenders

- Second Florida Homes

CASHOUT FLORIDA NO TAX RETURN Condotel MORTGAGE LENDERS

• Cashout Maximum Loan to value is 80% of appraisal value with 740+ credit score, otherwise 75% cashout Florida Condotel Condotel – Condotel , Condotel tels.

• Up to $3,000,000 cash out Florida permitted less any Florida mortgage payoffs

• Paying off a non-purchase money 2nd mortgage is defined as cash-out

• No ownership seasoning required but must have settlement statement for the purchase

• Source and seasoning required if Florida purchased within the prior 6 months.

• Proceeds from Florida cash-out can be used for cashout refinance reserve requirement.

• Power of Attorney not allowed for Condotel – Condotel , Condotel , cash-out refinances!

FLORIDA Condotel – Condotel RESERVE REQUIREMENTS

• Current reserve balance meets or exceeds 2 months of the Florida property’s HOA dues in reserves multiplied by all units in the Florida project or 10% or more reserve allocation designated in the most recent budget.

SECOND FLORIDA Condotel HOMES

• Florida mortgage lenders will typically define a property as a second Florida home if it is (1) located in a vacation or resort area 30 or more miles from the primary residence or (2) used a college housing for enrolled dependent within 5 miles of campus)

• Short-term Florida Florida rental income is allowed on second Florida homes and generally does not constitute an investment Florida property designation. Florida rental income cannot be used to qualify. An evaluation of the 1040 Schedule E is required.

FLORIDA Condotel INVESTMENT

• Property titled in LLC allowed (see Florida Mortgage Applicants and Title section for details)

• Maximum 60% LTV

• Gross Florida rental income is calculated by using a 12 month average of the net Schedule E income (Line 21) plus depreciation,

mortgage interest paid to banks, taxes and insurance, and HOA dues.

• Florida rental income not appearing on Schedule E may be considered case-by-case with 3 months canceled checks and a

current lease agreement. Use 75% of gross rent as gross Florida rental income.

• Immediate Florida rental income on the purchase of an investment property is allowed using 75% of the monthly rent schedule as documented by Form 1007 or 1025.

• Cash-out is allowed up to $4,000,000 with no seasoning required.

FLORIDA Condotel – MORTGAGE LENDERS – Florida Condotel lenders will define a Condotel unit as a Condotel when units in the complex can be reserved for daily, weekly or short-term Florida rentals.

• Maximum Florida Condotel 75% Loan to Value

• Leaseholds allowed if the remaining term on a land lease is 30 years or longer

FLORIDA Condotel –

– Blackout dates not permitting year-round owner occupancy

– Structural deficiencies and certain pending litigation (please contact your AE if litigation is not related

to a structural issue)

– Incomplete construction of the subject phase

Approved/Evaluated Case-by-Case:

– Low HOA budget reserves

– HOA delinquencies exceeding 15%

• Florida Condotel lenders questionnaire must be 100% complete for Approval Commitment. No blanks or questions answered “n/a” or “unknown,” and the questionnaire must pass underwriter review.

• Must have a full kitchen and at least one separate bedroom. Minimum 500 square feet is generally required. Efficiency or studio units are not permitted.

• Coinsurance is considered case-by-case if no agreed amount endorsement is available

Florida Condotel lenders will define a Condotel unit as a Condotel when units in the complex can be reserved for daily,

weekly or short-term Florida rentals.

MORTGAGE LENDERS TERMS- The ARM is a 1st mortgage adjustable rate loan with principal and interest payments amortized over 30 years.

- 30 Year fixed for 30 years..

FLORIDA Condotel MORTGAGE LENDER’S APPROVAL PROCESS

FLORIDA Condotel MINIMUM & MAX LOAN AMOUNTS

• $100,000 minimum loan amount. Exceptions are considered on a case-by-case.

• Co0OP Loan amount exceptions over $4,000,000 available.

FLORIDA Condotel MORTGAGE LENDERS CREDIT REQUIREMENTS

• 680 middle scores required with some exceptions allowed for lack of credit or unestablished credit.

• For co-Condotel – Condotel mortgage applicants and co-mortgagers, the lowest mid-score is used for pricing and qualification.

• Meeting the minimum credit score requirement does not automatically constitute a credit approval. A pattern of

adverse credit or overextended credit may disqualify Condotel – Condotel mortgage applicant from financing, even if the minimum credit score is met.

• Credit report is used for Pre-Approval and Condotel – Condotel mortgage lenders will also pull credit before issuing a conditional

approval. Mid-score from Condotel – Condotel mortgage lenders credit pull is used for pricing and qualification.

No Credit or Limited Credit

• No credit or limited credit profiles are allowed on a case-by-case basis for U.S. citizens.

• No U.S. credit or credit score is required for the Work Visa/Expatriate/Immigrant Program or Foreign National Program

FLORIDA Condotel MORTGAGE LENDERS OPTIONS INCLUDE:

- Primary Florida Condotel Mortgage Lenders

- Second Home Florida Condotel Mortgage Lenders

- Investments Florida Condotel Mortgage Lenders

- Cash Out Florida Condotel Refinancing

- Second Florida Condotel Home Financing

- Jumbo Florida Condotel Loans

- Low Florida Condotel Closing Costs

- Up to 80 Percent of Florida Condotel – Condotel Mortgage Loans

FLORIDA Condotel MORTGAGE MAXIMUM DEBT TO INCOME

Maximum Florida Condotel – Condotel Mortgage Lenders Debt To Income Ratio

• 43% maximum back-end ratio.

ELIGIBLE FLORIDA Condotel PROPERTY TYPES & OCCUPANCY

Florida Condotel – Condotel Occupancy Permitted

• Primary Florida Condotel – Condotel Residence

• Second Florida Condotel – Condotel Home (minimal Florida rental income allowed)

• Investment Florida Condotel – Condotel Property (non-owner Florida Condotel – Condotel occupied) permitted at maximum Florida Condotel – Condotel loan of 60% LTV

ELIGIBLE FLORIDA Condotel MORTGAGE REQUIREMENTS

• Minimum Down Payment 20% For Florida Condotel – Condotel Mortgage Lenders

• Title Insurance for Florida Condotel – Condotel s title policy issued through a title company or closing attorney must be issued on Florida Condotel – Condotel certificate

• Leaseholds Florida Condotel – Condotel allowed on a case-by-case basis

BAD CREDIT FLORIDA Condotel MORTGAGE LENDERS CREDIT REQUIREMENTS

• Late payments on any mortgage, installment or revolving account of 2×30, 1×60 or more will typically disqualify a

Florida Mortgage Applicants from financing. Exceptions will be reviewed on a case-by-case basis at a lower LTV.

• A pattern of adverse credit or overextended credit may disqualify Florida Mortgage Applicants from financing, even if the minimum credit score

is met. Florida Mortgage Applicants with 3x monthly income amount in unsecured consumer debt are generally disqualified.

FLORIDA Condotel MORTGAGE LENDERS REQUIREMENTS AFTER FORECLOSURE, BANKRUPTCY, SHORT SALE

• (4)Four-year seasoning from BK discharge date or sale of property

• Maximum 60% LTV or 40% downpayment

• No derogatory credit allowed since the bad credit event

• Strong extenuating circumstance and signed letter of explanation from Condotel – Condotel mortgage applicant detailing event required.

NOT ALLOWABLE FOR FLORIDA Condotel MORTGAGE LENDERS

– Structural Florida Condotel – Condotel deficiencies and certain pending litigation (please contact your AE if litigation is not related to a structural issue)

– Incomplete Florida Condotel – Condotel construction of the subject phase

APPROVED OR ALLOWED FLORIDA Condotel MORTGAGE LENDERS CASE BY CASE:

– Low Florida Condotel – Condotel HOA budget reserves

– HOA Florida Condotel – Condotel delinquencies exceeding 15%

• Florida Condotel – Condotel mortgage lenders Questionnaire must be 100% complete for Approval Commitment. No blanks or questions answered “n/a” or “unknown,” and the Florida Condotel – Condotel questionnaire must pass underwriter review.

• Florida Condotel – Condotel s mortgage lenders price Florida Condotel – Condotel s the same as Non-Warrantable Condotel s, regardless of loan size or Florida Condotel – Condotel questionnaire findings.

• Florida Condotel – Condotel must pust have a full kitchen and at least one separate bedroom. Minimum Florida Condotel – Condotel size 500 square feet generally required. Efficiency Florida Condotel – Condotel s or studio units are not permitted.

• Coinsurance Florida Condotel – Condotel is considered case-by-case if no agreed amount endorsement is available.

SELF-EMPLOYED FLORIDA Condotel MORTGAGE LENDERS

Self-Employed Condotel – Condotel mortgage Income calculations

• Florida Mortgage Applicants should be self-employed in the U.S. for a minimum of 2 years (max 80% LTV).

• 2-years business & personal tax returns required, plus year-to-date Profit & Loss statement.

• Business tax returns required for all businesses in which the Florida Mortgage Applicants has 25% ownership or more. On occasion

business tax returns are needed if the Florida Mortgage Applicants is has less than 25% ownership.

• Fannie Mae cash flow analysis form can be used.

• NOL Carryover Loss: Treated case-by-case when truly a one-time occurrence (i.e. real estate loss, lawsuit settlement or some other form of a truly one-time occurrence). Detailed CPA letter addressing the one-time occurrence is required.

• Less than two years self-employment is considered on a case-by-case basis with a reduced LTV.

REQUIRED BY FLORIDA Condotel MORTGAGE LENDERS

• 2-months bank statements for monthly asset accounts, and most recent statement for quarterly asset accounts

(VOD not permitted).

• 6 months PITI for all Florida Condotel – Condotel properties owned including subject.

• At least 3 months of the subject property’s reserves must be liquid non-retirement.

FLORIDA Condotel MORTGAGE LENDERS CASE BY CASE MORTGAGE APPROVALS

• Florida Condotel – Condotel Current reserve balance meets or exceeds 2 months of the subject property’s Florida Condotel – Condotel HOA dues in reserves multiplied by all Florida Condotel – Condotel units in the Florida Condotel – Condotel project or 10% or more reserve allocation designated in the most recent Florida Condotel – Condotel budget.

SECOND HOME FLORIDA Condotel MORTGAGE LENDERS

• Florida Condotel – Condotel Mortgage Lenders will typically define a property as a second Florida Condotel – Condotel home if it is (1) located in a vacation or resort area 30 or more miles from the primary Florida Condotel – Condotel residence or (2) used a Florida Condotel – Condotel college housing for enrolled dependent within 5 miles of campus)

• Short-term Florida Condotel – Condotel Florida rental income is allowed on second Florida Condotel – Condotel homes and generally does not constitute a Florida Condotel – Condotel investment property designation. Florida Condotel – Condotel Florida rental income cannot be used to qualify. An evaluation of the 1040 Schedule E is required.

FLORIDA Condotel MORTGAGE FOR INVESTMENT PROPERTY

• Property titled in LLC allowed

• Maximum Florida Condotel – Condotel 60% LTV for investor Florida Condotel – Condotel mortgage lenders.

• Gross Florida rental income is calculated by using a 12 month average of the net Schedule E income (Line 21) plus depreciation, mortgage interest paid to banks, taxes and insurance, and Florida Condotel – Condotel HOA dues.

• Florida rental income not appearing on Schedule E may be considered case-by-case with 3 months canceled checks and a current lease agreement. Use 75% of gross rent as gross Florida rental income.

• Immediate Florida Condotel – Condotel Florida rental income on the purchase of an investment property is allowed using 75% of the monthly rent schedule as documented by Form 1007 or 1025.

• Cash-out is allowed up to $3,000,000 with no seasoning required.

WHAT IS A FLORIDA Condotel AND HOW DO I GET A FLORIDA MORTGAGE?

A Florida Condotel – Condotel or Condotel erative apartment is an individual living unit within a Florida Condotel – Condotel building or development where a buyer purchases shares (equal to the value of the unit) in a Florida Condotel – Condotel corporation that holds title to a building Condotel s are predominantly located. Normally a Florida Condotel – Condotel sponsor will buy the building (takes out the underlying Florida Condotel – Condotel mortgage) and then will sell off the shares. Therefore, when buying a Condotel , you are actually buying Florida Condotel – Condotel shares in a corporation, not buying real property.

HOW TO FLORIDA Condotel BUILDINGS GET PRE QUALIFIED BY FLORIDA MORTGAGE LENDERS?

To start with Florida Condotel – Condotel lender will look at the following factors to see if a particular Florida Condotel – Condotel building corresponds with their guidelines: the Florida Condotel – Condotel property’s resale value, investor concentration, and Florida Condotel – Condotel owner occupancy. Based on the previous example, if there are 20 units, five sponsor Florida rentals and 15 sold units (with 12 owner-occupied units and 3 units being rented by the Florida Condotel – Condotel owners), the following ratios and guideline percentages result:

HOW IS A FLORIDA DIFFERENT FROM A HOUSE OR Condotel ?

When you get a mortgage to purchase a house or Condotel you get the deed. But not with a Florida Condotel – Condotel , individual units do not have individual deeds. A Florida Condotel – Condotel mortgage is actually a “share-loan” or a loan that purchases a share within in the Florida Condotel – Condotel . The difference makes securing a loan for a Florida Condotel – Condotel more complicated them getting a traditional mortgage and fewer mortgage lenders offer share loans.

FLORIDA BOARDS AND APPROVAL RULES

To buy into a Florida Condotel – Condotel , you must be approved by the Florida Condotel – Condotel board. The approval process is often extensive and may require interviews and character references, in addition to your employment, financial, and credit history. Florida Condotel – Condotel boards can refuse a prospective buyer for any reason, so long as it doesn’t run afoul of anti-discrimination policies. What you can do WITH your Florida Condotel – Condotel unit. As a Florida Condotel – Condotel shareholder, you don’t have the right of alienation where basically, you can’t sell your Florida Condotel – Condotel share (or rent your Florida Condotel – Condotel unit) without the permission of the Florida Condotel – Condotel board. Some Florida Condotel – Condotel associations have the right of first refusal, meaning they have the option to buy the property before you offer your Florida Condotel – Condotel to outside buyers. Florida Condotel – Condotel boards, though, can simply deny a sale without matching the sale price.

HOW FLORIDA OWNERSHIP DIFFERS FROM Condotel OWNERSHIP

When you purchase a Condotel minium you are purchasing a specific unit the surface and the interior walls of the unit in the space the Condotel contains. With a Condotel – Condotel , you are purchasing a share in a corporation, which then entitles you to a unit. This share is considered personal property rather than real estate.

FLORIDA Condotel REFINANCE AFTER LISTED FOR SALE

Florida Condotel Condotel Mortgage Refinance of a Property Listed For Sale

• No Off-MLS seasoning requirement for borrower-paid compensation. Florida Condotel mortgage discount point fee is required. Condotel refinances ok if Home can remain listed For Sale.

• 90-days off the MLS required for lender-paid compensation

FLORIDACondotel NUMBER OF HOMES FINANCED

• The number of financed limited to 10 with some exceptions made for very high net worth borrowers. Please note reserve requirement applies to all properties owned (see Reserve Requirement & Rental Income sections).