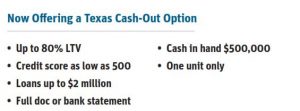

Up To 500K Texas Cash-Out Mortgage Lenders Up To 80% Min 500 Fico!

Texas Mortgage Lenders Loan Programs Include:

- Bad Texas Bad Texas Bad Credit Texas Mortgage Lenders

- FHA Texas Mortgage Lenders

- Self Employed Mortgage Lenders

- Stated Income Texas Mortgage Lenders

- VA Texas Mortgage Lenders

- Texas FHA Mortgage Lenders

Texas mortgage refinance WITH bad CREDIT

The presence of significant derogatory Texas Bad Texas Bad Credit events dramatically increases the likelihood of a future default and represents a significantly higher level of default risk. Examples of significant derogatory Texas Bad events include bankruptcies, foreclosures, deeds-in-lieu of foreclosure, preforeclosure sales, short sales, and charge-offs of mortgage accounts.

Note: The terms “preforeclosure sale” and “short sale” are used interchangeably in this Guide and have the same meaning (see Deed-in-Lieu of Foreclosure, Preforeclosure Sale, and Charge-Off of a Mortgage Account below).

The lender must determine the cause and significance of the derogatory information, verify that sufficient time has elapsed since the date of the last derogatory information, and confirm that the borrower has re-established an acceptable Texas Bad Texas Bad Credit history. The lender must make the final decision about the acceptability of a borrower’s Texas Bad Texas Bad Credit history when significant derogatory Texas Bad Texas Bad Credit information exists.

This topic describes the amount of time that must elapse (the “waiting period”) after a significant derogatory Texas Bad Texas Bad Credit event before the borrower is eligible for a new loan salable to Fannie Mae. The waiting period commences on the completion, discharge, or dismissal date (as applicable) of the derogatory Texas Bad Texas Bad Credit event and ends on the disbursement date of the new loan for manually underwritten loans. See B3-5.3-09, DU Texas Bad Texas Bad Credit Report Analysis, for additional information pertaining to DU loan case files, including how the waiting period is determined. Also see B3-5.3-08, Extenuating Circumstances for Derogatory Texas Bad Texas Bad Credit, for additional information.

Note: The requirements pertaining to significant derogatory Texas Bad Texas Bad Credit are not applicable to DU Refi Plus or Refi Plus mortgage loans. (See B5-5.2-02, DU Refi Plus and Refi Plus Underwriting Considerations.)

Identification of Significant Derogatory Texas Bad Credit Events

Lenders must review the Texas Bad Texas Bad Credit report and Section VIII, Declarations, of the loan application to identify instances of significant derogatory Texas Bad Texas Bad Credit events. Lenders must review the public records section of the Texas Bad Texas Bad Credit report and all tradelines, including mortgage accounts (first liens, second liens, home improvement loans, HELOCs, and manufactured home loans), to identify previous foreclosures, deeds-in-lieu, preforeclosure sales, charge-offs of mortgage accounts, and bankruptcies. Lenders must carefully review the current status of each tradeline, manner of payment codes, and remarks to identify these types of significant derogatory Texas Bad Texas Bad Credit events. Remarks Codes are descriptive text or codes that appear on a tradeline, such as “Foreclosure,” “Forfeit deed-in-lieu of foreclosure,” and “Settled for less than full balance.”

Significant derogatory Texas Bad Texas Bad Credit events may not be accurately reported or consistently reported in the same manner by all Texas Bad Texas Bad Creditors or Texas Bad Texas Bad Credit reporting agencies. If not clearly identified in the Texas Bad Texas Bad Credit report, the lender must obtain copies of appropriate documentation. The documentation must establish the completion date of a previous foreclosure, deed-in-lieu or preforeclosure sale, or date of the charge-off of a mortgage account; confirm the bankruptcy discharge or dismissal date; and identify debts that were not satisfied by the bankruptcy. Debts that were not satisfied by a bankruptcy must be paid off or have an acceptable, established repayment schedule.

Note: Timeshare accounts are considered installment loans and are not subject to the waiting periods described below.

Texas Mortgage After Bankruptcy (Chapter 7 or Chapter 11)

A four-year waiting period is required, measured from the discharge or dismissal date of the bankruptcy action.

Exceptions for Extenuating Circumstances

A two-year waiting period is permitted if extenuating circumstances can be documented, and is measured from the discharge or dismissal date of the bankruptcy action.

Texas mortgage refinance after Bankruptcy (Chapter 13)

A distinction is made between Chapter 13 bankruptcies that were discharged and those that were dismissed. The waiting period required for Chapter 13 bankruptcy actions is measured as follows:

- two years from the discharge date, or

- four years from the dismissal date.

The shorter waiting period based on the discharge date recognizes that borrowers have already met a portion of the waiting period within the time needed for the successful completion of a Chapter 13 plan and subsequent discharge. A borrower who was unable to complete the Chapter 13 plan and received a dismissal will be held to a four-year waiting period.

Exceptions for Extenuating Circumstances

A two-year waiting period is permitted after a Chapter 13 dismissal if extenuating circumstances can be documented. There are no exceptions permitted to the two-year waiting period after a Chapter 13 discharge.

TEXAS Mortgage after Multiple Bankruptcy Filings

For a borrower with more than one bankruptcy filing within the past seven years, a five-year waiting period is required, measured from the most recent dismissal or discharge date.

Note: The presence of multiple bankruptcies in the borrower’s Texas Bad Texas Bad Credit history is evidence of significant derogatory Texas Bad Texas Bad Credit and increases the likelihood of future default. Two or more borrowers with individual bankruptcies are not cumulative and do not constitute multiple bankruptcies. For example, if the borrower has one bankruptcy and the co-borrower has one bankruptcy this is not considered a multiple bankruptcies.

Exceptions for Extenuating Circumstances

A three-year waiting period is permitted if extenuating circumstances can be documented, and is measured from the most recent bankruptcy discharge or dismissal date. The most recent bankruptcy filing must have been the result of extenuating circumstances.

texas mortgage after Foreclosure

A seven-year waiting period is required, and is measured from the completion date of the foreclosure action as reported on the Texas Bad Texas Bad Credit report or other foreclosure documents provided by the borrower.

Exceptions for Extenuating Circumstances

A three-year waiting period is permitted if extenuating circumstances can be documented, and is measured from the completion date of the foreclosure action. Additional requirements apply between three and seven years, which include:

- Maximum LTV, CLTV, or HCLTV ratios of the lesser of 90% or the maximum LTV, CLTV, or HCLTV ratios for the transaction per the Eligibility Matrix.

- The purchase of a principal residence is permitted.

- Limited cash-out refinances are permitted for all occupancy types pursuant to the eligibility requirements in effect at that time.

Note: The purchase of second homes or investment properties and cash-out refinances (any occupancy type) are not permitted until a seven-year waiting period has elapsed.

TEXASForeclosure and Bankruptcy on the Same Mortgage

If a mortgage debt was discharged through a bankruptcy, the bankruptcy waiting periods may be applied if the lender obtains the appropriate documentation to verify that the mortgage obligation was discharged in the bankruptcy. Otherwise, the greater of the applicable bankruptcy or foreclosure waiting periods must be applied.

Deed-in-Lieu of Foreclosure, Preforeclosure Sale, and Charge-Off of a Mortgage Account

These transaction types are completed as alternatives to foreclosure.

- A deed-in-lieu of foreclosure is a transaction in which the deed to the real property is transferred back to the servicer. These are typically identified on the Texas Bad Texas Bad Credit report through Remarks Codes such as “Forfeit deed-in-lieu of foreclosure.”

- A pre-foreclosure sale or short sale is the sale of a property in lieu of a foreclosure resulting in a payoff of less than the total amount owed, which was pre-approved by the servicer. These are typically identified on the Texas Bad Texas Bad Credit report through Remarks Codes such as “Settled for less than full balance.”

- A charge-off of a mortgage account occurs when a Texas Bad Texas Bad Creditor has determined that there is little (or no) likelihood that the mortgage debt will be collected. A charge-off is typically reported after an account reaches a certain delinquency status, and is identified on the Texas Bad Texas Bad Credit report with a manner of payment (MOP) code of “9.”

A four-year waiting period is required from the completion date of the deed-in-lieu of foreclosure, preforeclosure sale, or charge-off as reported on the Texas Bad Texas Bad Credit report or other documents provided by the borrower.

Exceptions for Extenuating Circumstances

A two-year waiting period is permitted if extenuating circumstances can be documented.

Note: Deeds-in-lieu and preforeclosure sales may not be accurately or consistently reported in the same manner by all Texas Bad Texas Bad Creditors or Texas Bad Texas Bad Credit reporting agencies. See Identification of Significant Derogatory Texas Bad Texas Bad Credit Events in the Texas Bad Texas Bad Credit Report above for additional information.

Texas Bad Texas Bad Credit Requirements for Re-establishing

After a bankruptcy, foreclosure, deed-in-lieu of foreclosure, preforeclosure sale, or charge-off of a mortgage account, the borrower’s Texas Bad Texas Bad Credit will be considered re-established if all of the following are met:

- The waiting period and the related additional requirements are met.

- The loan receives a recommendation from DU that is acceptable for delivery to Fannie Mae or, if manually underwritten, meets the minimum Texas Bad Texas Bad Credit score requirements based on the parameters of the loan and the established eligibility requirements.

- The borrower has a traditional Texas Bad Texas Bad Credit as outlined in within Section, Traditional Texas Bad Texas Bad Credit History. Nontraditional Texas Bad Texas Bad Credit or “thin files” are not acceptable.

Summary BAD CREDIT TEXAS FANNIE MAE WAIT TIMES

The following table summarizes the waiting period requirements for all significant derogatory Texas Bad Texas Bad Credit events.

| Derogatory Event | Waiting Period Requirements | Waiting Period with Extenuating Circumstances |

|---|---|---|

| Texas Bankruptcy — Chapter 7 or 11 | 4 years | 2 years |

| Texas Bankruptcy — Chapter 13 |

|

|

| Multiple Texas Bankruptcy Filings | 5 years if more than one filing within the past 7 years | 3 years from the most recent discharge or dismissal date |

| Texas Foreclosure1 | 7 years | 3 yearsAdditional requirements after 3 years up to 7 years:

|

| Deed-in-Lieu of Foreclosure, Preforeclosure Sale, or Charge-Off of Mortgage Account | 4 years | 2 years |