1099 Texas Mortgage Lenders – No Tax Returns – No Bank Statements

- 2 YEARS 1099S

- SELF PREPARED MOST RECENT 24 MONTHS PROFIT AND LOSS STATEMENT.

- NO TAX RETURNS NEEDED

- NO BANK STATEMENTS NEEDED FOR INCOME

File Form 1099 Mortgage Lenders-can use 1099 only for each person to whom you have paid during the year. Self-employed Contractors are issued 1099 if they:

- at least $10 in royalties or broker payments in lieu of dividends or tax-exempt interest;

- at least $600 in:

- rents;

- services performed by a 1099 contractor someone who is not your employee;

- Earn 1099 contractor prizes and awards;

- Earn 1099 contractor other income payments;

- Earn 1099 contractor medical and health care payments;

- Earn 1099 contractor crop insurance proceeds;

- Earn 1099 contractor cash payments for fish you purchase from anyone engaged in the trade or business of catching fish;

- Earn 1099 contractor or cash paid from a notional principal contract to an individual, partnership, or estate;

- payments to an attorney; or

- Earn 1099 contractor from any other type of contractor work.

- In addition, use this form to report that you made direct sales of at least $5,000 of consumer products to a buyer for resale anywhere other than a permanent retail establishment.

-

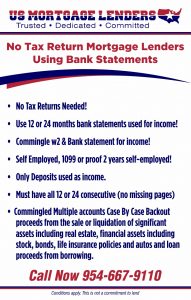

TEXAS BANK STATEMENT ONLY MORTGAGE LENDERS THAT ONLY NEED 1099’S:

- 1099 Only Texas Mortgage Lenders – 2 Years Self Employed Required!

- 1099 Only Texas Mortgage Lenders – Last 2 years 1099a used to qualify!

- 1099 Only Texas Mortgage Lenders – No tax returns required

- 1099 Only Texas Mortgage Lenders – NO Business Or Personal Tax Returns Needed!(Personal and Business)

- 1099 Only Texas Mortgage Lenders – Loans up to $3 million

- 1099 Only Texas Mortgage Lenders – Credit scores down to 600

- 1099 Only Texas Mortgage Lenders – Credit scores down to 500 if mortgage payments timely

- 1099 Only Texas Mortgage Lenders – Up to 85% LTV

- 1099 Only Texas Mortgage Lenders – DTI up to 55% considered

- 1099 Only Texas Mortgage Lenders – Owner-occupied, 2nd homes, and investment properties

- 1099 Only Texas Mortgage Lenders – 1 day seasoning for foreclosure, short sale, BK, DIL

- 1099 Only Texas Mortgage Lenders – Non-warrantable condos considered

- 1099 Only Texas Mortgage Lenders – Jumbo loans down to 660 score

- 1099 Only Texas Mortgage Lenders – 5/1 ARM or 30-year fixed

- 1099 Only Texas Mortgage Lenders – No Pre-payment penalty for owner-occ and 2nd homes

- 1099 Only Texas Mortgage Lenders – SFRs, townhomes, condos, 2-4 units

- 1099 Only Texas Mortgage Lenders – Seller concessions to 6% (2% for investment)

6 TEXAS STATED INCOME MORTGAGE LENDERS PROGRAMS

Our W-2 Only Texas Mortgage Program is for Texas home Buyers that have filed 2106 expenses & as a result do not qualify for a home loan.

W2 Transcripts Program Guidelines

- Applicable to Conventional, FHA and VA loans up to $625,500 subject to Texas county limits excluding Homepath.

- W-2’s & Current Paystubs.

- No Tax Returns Required

- NOTE: If Borrower has any other income such as Scheduled C or E they are NOT eligible for this program

- ALSO: Borrower’s that earn 25% or more of their income from commission will NOT qualify for this program

- Signed 4506 required (we will Only run W-2 transcripts)

- FHA / Conventional & VA Loans up to $625,000 (subject to county limits)

- Purchases & Refinances

Our W-2 Only Texas Mortgage Program is for Texas home Buyers that have filed 2106 expenses & as a result do not qualify for a home loan.

Fast Consultation

If you are a Texas W2 employee and you’re trying to buy a Texas home with too many tax deductions you might have a problem. Texas home buyers learn quickly that if they take advantage of to many unreimbursed expenses on their tax returns that include meals, computers, uniforms, cell phone usage, travel or other related or not work related expenses the expenses are considered unreimbursed employee expenses. Too many unreimbursed deductions can lower your Texas home buying purchasing power.

Throughout the year Texas w2 employees write off expenses in order to deduct or write off their income. Your w2 write offs lower your taxable income so at the end of the year you you have a lower taxable income.

Where Texas home buyers write off unreimbursement employee expenses?

As a W2 employee you will find all of your unreimbursed employee expenses on line 21 of your Schedule A – this is part of your federal tax return.

How do these unreimbursed expenses impact my income for purchasing a home?

When looking at line 21 of your Schedule A you will see your annual employee expenses. This amount will include any of the expenses you have incurred as a direct result of your job.

Everything in the world of mortgages is calculated monthly so let’s breakdown the numbers:

• Annual Gross Income………………………… $50,000

• Annual Employee Reimbursement Expenses.. $20,000

• Annual Taxable income ……………………..$30,000 /12=

• Final Monthly Mortgage Qualifying Income…..$2500

Ok so what’s the problem? Lenders don’t like to extend borrowers Debt to income ratio beyond the standard 35% towards the housing expense.

www.Texas-Mortgage-Lenders.com

What do debt-to-income ratios have to do with my mortgage? Debt-to-income ratios (DTI) are used to ensure you can afford to pay your mortgage along with other monthly debts you may be paying (such as a car payment). There is a front and back ratio – the formula is simple math:

Monthly Mortgage Payment / Gross Monthly Income = Front DTI

Your front DTI shows your income can sustain just the mortgage with taxes, insurance and any condo assessments.

Monthly Mortgage Payment + Monthly Debt / Gross Monthly Income = Back DTI

Your back DTI shows you income can sustain the mortgage in addition to other monthly obligations (only those found on your credit report).

It’s rare your W2 unreimbursed employee expenses will prevent you from buying a home; however, if your back debt-to-income ratio (DTI) is nearing the average limit of 45 percent your deductions can push your percentages over the ideal threshold and can create some challenges.

It’s difficult to speculate on every loan scenario so understand that these challenges can typically be resolved by simply lowering your monthly debt or using a lender with more flexible lending guidelines.

So what’s the bottom line?

On average, any of these unreimbursed employee expenses will be minimal, yet still worth mentioning to your Texas mortgage professional during the Texas mortgage loan preapproval process. So Which Deductions Can Be Itemized?

Schedule A is broken down into several different sections that deals with each type of Texas itemized deduction. For a breakdown of your itemized deductions, see the IRS instructions for Schedule A.

The following is a brief overview of the scope and limits of each category of itemized deduction:

- Unreimbursed Texas Medical and Dental Expenses – This deduction is perhaps the most difficult – and financially painful – to qualify for. Taxpayers that incur qualified out-of-pocket medical and/or dental expenses that are not covered by insurance can deduct expenses that exceed 7.5% of their adjusted gross incomes.

- Interest Expenses – Homeowners can deduct the interest that they pay on their mortgages and home equity lines of credit.

Each year, mortgage lenders mail Form 1098 to Texas borrowers, which details the exact amount of deductible interest and points that they’ve paid over the past year. Taxpayers that bought or refinanced homes during the year can also deduct the points that they’ve paid, within certain guidelines.

- Taxes Paid – Taxpayers who itemize are able to deduct two types of taxes paid on their Schedule A. Personal property taxes, which include real estate taxes, are deductible along with state and local taxes that were assessed for the previous year. However, any refund that was received by the taxpayer from the state in the previous year must be counted as income if the taxpayer itemized deductions in the previous year.

- Charitable Texas Donations – Any donation made to a qualified charity is deductible within certain limitations. Cash contributions that exceed 50% of the taxpayer’s adjusted gross income must be carried over to the next year, as well as noncash contributions that exceed 30% of AGI. (Keep reading about donations in Deducting Your Donations and It Is Better To Give AND Receive.)

- Casualty and Theft Losses – Any loss incurred as a result of a casualty or theft can be reported on the Schedule A. Unfortunately, only losses in excess of 10% of the taxpayer’s adjusted gross income are actually deductible. If a taxpayer incurs a casualty loss in one year and deducts it on his or her taxes, then any reimbursement that is received in later years must be counted as income. Casualty losses are carried on to the Schedule A from IRS Form 4864.

- Unreimbursed Texas Job-Related Expenses and Certain Miscellaneous Deductions – W-2 employees that incur work-related expenses can deduct any aggregated expenditures that exceed 2% of their adjusted gross incomes. These include items such as equipment and supplies, protective clothing, expenses for maintaining a home office for the convenience of the employer, vehicle expenses, dues to professional organizations and professional subscriptions. Certain other miscellaneous deductions are listed in this section as well, such as income tax preparation and audit fees and any expenses related to maintaining investments or income-producing property. These fees include such things as IRA or other account maintenance fees paid out of pocket, legal and accounting fees, and margin interest.

- Other Miscellaneous Texas tax Deductions – This final category of IRS itemized deductions includes items such as gambling losses to the extent of gambling winnings, losses from partnerships or subchapter S-corporations, estate taxes on income in respect of a decedent and certain other expenses. For additional details, see IRS Publication 17 and the instructions for Schedule A.