Self Employed Florida Mortgage Lenders

Bank Statement loans for self-employed borrowers who cannot qualify for a traditional bank loan because of business expenses. Self-employed Florida mortgage Lenders are perfect because while most Florida self-employed borrowers earn a solid income, they show a smaller net income on their tax returns. Our Florida mortgage team is well-versed in these bank statement only loans and placing the borrowers where they can get the optimal loan to fit their needs

Self Employed Florida Bank Statment Lenders Summary

Florida Self Employed Advantages Include

About Florida Self Employed Mortgage Lenders

If you’re one of the 1000’s of Florida self-employed workers that write off to much income to qualify for a Florida mortgage? it is now easier than ever to be self-employed get approved for a Florida mortgage if you are self-employed and have sufficient income and payment history you can now qualify for a bank statement only Florida mortgage. Fannie Mae has relaxed some of their guidelines for documenting self-employed income. Even today Florida self-employed mortgage applicants are having trouble betting approve for their Florida dream home. Here we have provided the much-needed information to help you get approved for a self-employed mortgage loan using bank statements only to document your income and ability to make the Florida mortgage payments.

How Long Must You Be Self Employed in Florida To Qualify?

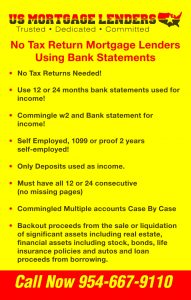

Most Florida mortgage lenders that provide self-employed mortgage loans want to see proof of at least 2 years business history. Some Florida self-employed mortgage lenders only require 12 months personal bank statements but still want proof of stability for at least 2 years. For self-employed Florida business owners using business bank statements 24 months business bank statements are required and a Florida profit and loss statement signed by the Florida business. NO Tax Returns Needed!

SELF EMPLOYED FLORIDA MORTGAGE APPLICANTS CAN NOW QUALIFY FOR LESS THAN 2 YEARS SELF EMPLOYED!Here’s more good news for our Self Employed Mortgage Applicants! Self Employed Florida Mortgage Lenders Home Loans, Inc. may be able to approve your self-employed borrowers, even those with a history with less than two years of self-employment. These applicants may qualify for our Fresh Start, Homeowner’s Access and Premier Access products. When qualifying these borrowers, our underwriters look for:

|

Self Employed Income Using Tax Returns Make it Hard To Qualify

A borrower’s income is still probably the single most important factor in qualifying for a Florida mortgage. For traditional Florida mortgage lenders to know what you earn, they will want to see at least the last two-years of a self-employed borrower’s Schedule C from an IRS Form 1040. Schedule C is the tax form that represents the income or loss from your Florida business. If income increases between year one and year two, Florida mortgage lenders will take an average of the two years. However, if the second year’s most recent income is lower than the first year, Florida mortgage lenders are required to use the lower number. With our bank statement only mortgage program this is not an issue because the lender will add u p your most recent 12 or 24 months bank statements and average out your income.

Self Employed Florida Mortgage Loans

If you’re going to mortgage your Florida home purchase with traditional financing that is conforming to Fannie Mae and Freddie Mac guidelines you will be required to fully document your self-employment income via adjusted income on your 1040 tax returns. It is standard that Fannie Mae will want a full 2 years worth of tax returns to document your net income after expenses. For many Florida self-employed mortgage applicants to provide this requirement can be difficult for self-employed Florida business owners.

If you’re purchasing a new Florida home or refinancing your existing Florida mortgage there is a specific process Florida self-employed must go through to get approved for a Florida mortgage. Under the old guidelines, self-employed works had difficulty qualifying based on proof of income. This happens for a variety of reasons including how a business is structured most importantly how much income you write off as a self-employed Florida mortgage applicant.

Florida self-employed workers have no history of paychecks that can be documented because the employer usually pays the w2 employee expenses. They take may take distributions with no regular amount or frequency making qualifying based on income difficult even with bank statements and tax returns. If your business is new and you don’t have documented sources of revenue or even two years of federal tax returns this can make qualifying for a traditional mortgage difficult, if not impossible.

If you have a history of paying yourself from your Florida business, Fannie Mae’s guidelines state that your business only needs to have adequate income to support your future distributions. Most Florida mortgage lenders will require documentation that your Florida business is legitimate and stable. This could be provided in the form of your letters of incorporation or the K-1 filing which highlights your percent Florida business ownership.

The underwriting process is still going to be more complicated for Florida self-employed mortgage applicants. Fannie Mae and Freddie Mac have similar processes to verify income from Florida self-employment.These requirements follow the ability to repay guidelines to ensure that you have adequate income from Florida business owners ability to repay the loan. Florida mortgage lenders adhere strictly to these guidelines so that the loans can be sold to Fannie Mae and Freddie Mac.

If you don’t have two years of business tax returns the guidelines you may be able to qualify for a bank statement program using your personal bank statements as an alternative to a conventional mortgage. These types of programs are available from boutique portfolio lenders and offer reasonable rates and fees.

Roadblocks for Florida Self Employed Mortgage Applicants

The most common roadblock Florida self-employed workers face is proving how much your net income is from the business based on tax returns and deductions. Florida self-employed mortgage applicants may have significant cash flow in your business but could be in for a shock when you learn your qualified net income based on tax write-offs and expenses for your business. If you cannot demonstrate sufficient net income from your business it still may be possible to qualify for a bank statement program using income on your personal statements.

Florida Business Tax Deductions Lower Documented Income

Running a business as a self-employed worker can be very expensive and often comes with significant tax liability. The temptation can be to lower your taxable income with deductions. These deductions include business expenses for things like equipment, expense accounts, and annual depreciation.

Taking business deductions may save you money on your taxes but it could make it more difficult to qualify for a mortgage. As a self-employed worker, you are qualified for a mortgage based on your net income, not gross income for a traditional worker.

Most self-employed business owners claim as many tax deductions as the law allows which significantly lowers your net income and therefore your ability to qualify for self-employed home loans.

Debt to Income Ratio for the Florida Self Employed

Maintaining a low debt to income ratio is important in qualifying for any mortgage loan. As a self-employed worker, your debt to income ratio is calculated differently from traditional workers.

Your debt ratio is calculated by your average net income from the most recent tax returns along with current year income and expenses. In order to be approved for a self-employment mortgage, your debt-to-income ratio cannot be more than 43 percent.

If you’re considering purchasing a new home or refinancing your existing mortgage you might want to consider taking fewer tax deductions to reduce your debt-to-income rate with the highest possible net income.

Florida Mortgage Documentation Makes a Difference

The loan process you’ll go through as a self-employed business owner is the same as everyone else. Where it gets sticky is providing your income documentation. The more you have to prove that business income is sustainable and able to pay the easier the process becomes to qualify as a self-employed Florida business owner.

Keeping accurate records of income and expenses will make it easier to prove that you are a sustainable business as well as documenting net income which is required for maintaining a favorable debt ratio.

Mortgages for Florida Self Employed Business Owners

Florida Mortgage lenders generally consider self-employed business owners to be higher risk than those who work for a traditional paycheck. Higher risk Self-employed Florida business owners pay more at closing and over the life the loan with higher interest rates. If you’re accepting a higher interest rate when you purchase your Florida home you may be able to lower that rate down the road by demonstrating a reliable payment history and refinancing.

How You Structure Your Florida Business Matters

There are several different ways to be self-employed and underwriters treat them all differently. The most common business structures include sole proprietorship, partnerships, LLCs and S corporations.

Under a sole proprietorship, your business income is reported on schedule c of your tax return. With a partnership profits in the business are split between partners based on their respective percent of ownership. Limited Liability Corporations are considered pass-through entities for tax purposes. S corporations follow strict guidelines for distributions. Depending on how you structure your business you could potentially pay yourself on a w-2 and avoid the hurdles of a self-employed mortgage completely. Your accountant can help you choose the optimal business structure for your company.

No matter how you choose to structure your business there are steps you can take to maximize your income from self-employment and maintain an optimal debt ratio. All of these factors are under you control and are part of maintaining healthy finances as a self-employed worker.

Florida Mortgage With Repossession On Credit Approvals!USE EQUITY IN LEASE PURCHASE FOR FLORIDA MORTGAGEFlorida Mortgage Approved after RepossessionFLORIDA MORTGAGE DEBT CONSOLIDATION REFINANCEFLORIDA MORTGAGE DEBT CONSOLIDATION REFINANCEFLORIDA DEBT CONSOLIDATION MORTGAGE REFINANCEFLORIDA COMMERCIAL HARD MONEY LENDERSAIRBNB-VRBO-HOME AWAY-FLORIDA MORTGAGE LENDERSFLORIDA MORTGAGE LENDERS USE INCOME BASED REPAY CALCULATIONSelf Employed Florida Mortgage LendersStudent-loan To Debts To High? YES – QUALIFY FOR A FLORIDA MORTGAGEFlorida Mortgage Lenders Non-Warrantable CondosFLORIDA SELF EMPLOYED MORTGAGE LENDERS- WE SAY YES!FLORIDA NON-WARRANTABLE CONDO LENDERS –10% DOWN + SELF EMPLOYED FLORIDA MORTGAGE LENDERS JUMBO BANK STATEMENT ONLY BAD CREDIT FLORIDA MORTGAGE LENDERSALAFIA FL Self Employed Mortgage LENDERSALTAMONTE SPRINGS FL Self Employed Mortgage LENDERSBankruptcy – Foreclosure – Short SaleFLORIDA Self Employed Mortgage LENDERS FOR ALL FLORIDAZUBER FL Self Employed Mortgage LENDERSZELLWOOD FL Self Employed Mortgage LENDERSYOUNGSTOWN FL Self Employed Mortgage LENDERSYELVINGTON FL Self Employed Mortgage LENDERSWINSTON FL Self Employed Mortgage LENDERSWINDSOR, ALACHUA COUNTY FL Self Employed Mortgage LENDERSWILLIS FL Self Employed Mortgage LENDERSWILLIFORD FL Self Employed Mortgage LENDERSWILCOX FL Self Employed Mortgage LENDERSWILCOX JUNCTION FL Self Employed Mortgage LENDERSWILBUR-BY-THE-SEA FL Self Employed Mortgage LENDERSWHITE CITY, GULF COUNTY FL Self Employed Mortgage LENDERSWHISPERING PINES FL Self Employed Mortgage LENDERSWESTCHESTER FL Self Employed Mortgage LENDERSWEST KENDALL FL Self Employed Mortgage LENDERSWELLBORN FL Self Employed Mortgage LENDERSWELCOME FL Self Employed Mortgage LENDERSWEIRSDALE FL Self Employed Mortgage LENDERSWAUKEENAH FL Self Employed Mortgage LENDERSWATERSOUND FL Self Employed Mortgage LENDERSWATERS LAKE FL Self Employed Mortgage LENDERSWATERCOLOR FL Self Employed Mortgage LENDERSWANNEE FL Self Employed Mortgage LENDERSWALNUT HILL FL Self Employed Mortgage LENDERSWAKULLA BEACH FL Self Employed Mortgage LENDERSWADESBORO FL Self Employed Mortgage LENDERSWACISSA FL Self Employed Mortgage LENDERSVOLUSIA FL Self Employed Mortgage LENDERSVIRGINIA VILLAGE FL Self Employed Mortgage LENDERSVINELAND FL Self Employed Mortgage LENDERSVIKING FL Self Employed Mortgage LENDERSVIERA FL Self Employed Mortgage LENDERSVERO LAKE ESTATES FL Self Employed Mortgage LENDERSVERMONT HEIGHTS FL Self Employed Mortgage LENDERSVERDIE FL Self Employed Mortgage LENDERSVENUS FL Self Employed Mortgage LENDERSVANDERBILT BEACH FL Self Employed Mortgage LENDERSVANDERBILT BEACH ESTATES FL Self Employed Mortgage LENDERSVALDEZ FL Self Employed Mortgage LENDERSUPTHEGROVE BEACH FL Self Employed Mortgage LENDERSUNIVERSITY, ORANGE COUNTY FL Self Employed Mortgage LENDERSTYLER FL Self Employed Mortgage LENDERSTWO EGG FL Self Employed Mortgage LENDERSTURKEY CREEK FL Self Employed Mortgage LENDERSTRILBY FL Self Employed Mortgage LENDERSTRILACOOCHEE FL Self Employed Mortgage LENDERSTRAIL CENTER FL Self Employed Mortgage LENDERSTHOMPSON FL Self Employed Mortgage LENDERSTERRA CEIA FL Self Employed Mortgage LENDERSTELOGIA FL Self Employed Mortgage LENDERSTAVERNIER FL Self Employed Mortgage LENDERSTARRYTOWN FL Self Employed Mortgage LENDERSTANGELO PARK FL Self Employed Mortgage LENDERSTALLEVAST FL Self Employed Mortgage LENDERSTAINTSVILLE FL Self Employed Mortgage LENDERSTAFT FL Self Employed Mortgage LENDERSSYDNEY FL Self Employed Mortgage LENDERSSWITZERLAND FL Self Employed Mortgage LENDERSSWEETWATER, HARDEE COUNTY FL Self Employed Mortgage LENDERSSWEETWATER CREEK FL Self Employed Mortgage LENDERSSWEET GUM HEAD FL Self Employed Mortgage LENDERSSVEA FL Self Employed Mortgage LENDERSSUWANNEE FL Self Employed Mortgage LENDERSSUNTREE FL Self Employed Mortgage LENDERSSUNSET POINT FL Self Employed Mortgage LENDERSSUNNYSIDE FL Self Employed Mortgage LENDERSSUNNY HILLS FL Self Employed Mortgage LENDERSSUN CITY FL Self Employed Mortgage LENDERSSUN ‘N LAKE OF SEBRING FL Self Employed Mortgage LENDERSSUMTERVILLE FL Self Employed Mortgage LENDERSSUMNER FL Self Employed Mortgage LENDERSSUMMERLAND KEY FL Self Employed Mortgage LENDERSSUMMERFIELD FL Self Employed Mortgage LENDERSSUMATRA FL Self Employed Mortgage LENDERSSUGARLOAF SHORES FL Self Employed Mortgage LENDERSSTOCK ISLAND FL Self Employed Mortgage LENDERSST. TERESA FL Self Employed Mortgage LENDERS ST. JOSEPH, PASCO COUNTY FL Self Employed Mortgage LENDERS ST. JOHNS FL Self Employed Mortgage LENDERS ST. JOHN FL Self Employed Mortgage LENDERS ST. HEBRON FL Self Employed Mortgage LENDERS ST. CATHERINE FL Self Employed Mortgage LENDERSSPUDS FL Self Employed Mortgage LENDERSSPRING LAKE, HIGHLANDS COUNTY FL Self Employed Mortgage LENDERSSPARR FL Self Employed Mortgage LENDERSSOUTHPORT FL Self Employed Mortgage LENDERSSOUTHFORT FL Self Employed Mortgage LENDERSSLAVIA FL Self Employed Mortgage LENDERSSILVER SPRINGS FL Self Employed Mortgage LENDERSSILVER PALM FL Self Employed Mortgage LENDERSSHELL POINT FL Self Employed Mortgage LENDERSSHADY GROVE, TAYLOR COUNTY FL Self Employed Mortgage LENDERSSHADY GROVE, JACKSON COUNTY FL Self Employed Mortgage LENDERSSHADEVILLE FL Self Employed Mortgage LENDERSSENYAH FL Self Employed Mortgage LENDERSSELMAN FL Self Employed Mortgage LENDERSSEASIDE FL Self Employed Mortgage LENDERSSEACREST FL Self Employed Mortgage LENDERSSCOTTSMOOR FL Self Employed Mortgage LENDERSSCOTTS FERRY FL Self Employed Mortgage LENDERSSCOTTOWN FL Self Employed Mortgage LENDERSSCOTLAND FL Self Employed Mortgage LENDERSSATSUMA FL Self Employed Mortgage LENDERSSANTA ROSA BEACH FL Self Employed Mortgage LENDERSSANTA MONICA FL Self Employed Mortgage LENDERSSANLANDO SPRINGS FL Self Employed Mortgage LENDERSSANDERSON FL Self Employed Mortgage LENDERSSAN MATEO FL Self Employed Mortgage LENDERSSAN CASTLE FL Self Employed Mortgage LENDERSSAMPSON CITY FL Self Employed Mortgage LENDERSSALT SPRINGS FL Self Employed Mortgage LENDERSSALEM FL Self Employed Mortgage LENDERSWASHINGTON COUNTY FL Self Employed Mortgage LENDERSWALTON COUNTY FL Self Employed Mortgage LENDERSWAKULLA COUNTY FL Self Employed Mortgage LENDERSVOLUSIA COUNTY FL Self Employed Mortgage LENDERSUNION COUNTY FL Self Employed Mortgage LENDERSTAYLOR COUNTY FL Self Employed Mortgage LENDERSSUWANNEE COUNTY FL Self Employed Mortgage LENDERSSUMTER COUNTY FL Self Employed Mortgage LENDERSST. LUCIE COUNTY FL Self Employed Mortgage LENDERS ST. JOHNS COUNTY FL Self Employed Mortgage LENDERSSEMINOLE COUNTY FL Self Employed Mortgage LENDERSSARASOTA COUNTY FL Self Employed Mortgage LENDERSSANTA ROSA COUNTY FL Self Employed Mortgage LENDERSPUTNAM COUNTY FL Self Employed Mortgage LENDERSPOLK COUNTY FL Self Employed Mortgage LENDERSPINELLAS COUNTY FL Self Employed Mortgage LENDERSPASCO COUNTY FL Self Employed Mortgage LENDERSPALM BEACH COUNTY FL Self Employed Mortgage LENDERSOSCEOLA COUNTY FL Self Employed Mortgage LENDERSORANGE COUNTY FL Self Employed Mortgage LENDERSOKEECHOBEE COUNTY FL Self Employed Mortgage LENDERSOKALOOSA COUNTY FL Self Employed Mortgage LENDERSNASSAU COUNTY FL Self Employed Mortgage LENDERSMONROE COUNTY FL Self Employed Mortgage LENDERSMIAMI-DADE COUNTY FL Self Employed Mortgage LENDERSMARTIN COUNTY FL Self Employed Mortgage LENDERSMARION COUNTY FL Self Employed Mortgage LENDERSMANATEE COUNTY FL Self Employed Mortgage LENDERSMADISON COUNTY FL Self Employed Mortgage LENDERSLIBERTY COUNTY FL Self Employed Mortgage LENDERSLEVY COUNTY FL Self Employed Mortgage LENDERSLEON COUNTY FL Self Employed Mortgage LENDERSLEE COUNTY FL Self Employed Mortgage LENDERSLAKE COUNTY FL Self Employed Mortgage LENDERSLAFAYETTE COUNTY FL Self Employed Mortgage LENDERSJEFFERSON COUNTY FL Self Employed Mortgage LENDERSJACKSON COUNTY FL Self Employed Mortgage LENDERSINDIAN RIVER COUNTY FL Self Employed Mortgage LENDERSHOLMES COUNTY FL Self Employed Mortgage LENDERSHILLSBOROUGH COUNTY FL Self Employed Mortgage LENDERSHIGHLANDS COUNTY FL Self Employed Mortgage LENDERSHERNANDO COUNTY FL Self Employed Mortgage LENDERSHENDRY COUNTY FL Self Employed Mortgage LENDERSHARDEE COUNTY FL Self Employed Mortgage LENDERSHAMILTON COUNTY FL Self Employed Mortgage LENDERSGULF COUNTY FL Self Employed Mortgage LENDERSGLADES COUNTY FL Self Employed Mortgage LENDERSGILCHRIST COUNTY FL Self Employed Mortgage LENDERSGADSDEN COUNTY FL Self Employed Mortgage LENDERSFRANKLIN COUNTY FL Self Employed Mortgage LENDERSFLAGLER COUNTY FL Self Employed Mortgage LENDERSESCAMBIA COUNTY FL Self Employed Mortgage LENDERSDUVAL COUNTY FL Self Employed Mortgage LENDERSDIXIE COUNTY FL Self Employed Mortgage LENDERSDESOTO COUNTY FL Self Employed Mortgage LENDERSCOLUMBIA COUNTY FL Self Employed Mortgage LENDERSCOLLIER COUNTY FL Self Employed Mortgage LENDERSCLAY COUNTY FL Self Employed Mortgage LENDERSCITRUS COUNTY FL Self Employed Mortgage LENDERSCHARLOTTE COUNTY FL Self Employed Mortgage LENDERSCALHOUN COUNTY FL Self Employed Mortgage LENDERSBROWARD COUNTY FL Self Employed Mortgage LENDERSBREVARD COUNTY FL Self Employed Mortgage LENDERSBRADFORD COUNTY FL Self Employed Mortgage LENDERSBAY COUNTY FL Self Employed Mortgage LENDERSBAKER COUNTY FL Self Employed Mortgage LENDERSALACHUA COUNTY FL Self Employed Mortgage LENDERSRUTLAND FL Self Employed Mortgage LENDERSRUNYON FL Self Employed Mortgage LENDERSROUND LAKE FL Self Employed Mortgage LENDERSROTONDA WEST FL Self Employed Mortgage LENDERSROSEMARY BEACH FL Self Employed Mortgage LENDERSROLLINS CORNER FL Self Employed Mortgage LENDERSROCKY CREEK FL Self Employed Mortgage LENDERSROCK HARBOR FL Self Employed Mortgage LENDERSROCHELLE FL Self Employed Mortgage LENDERSRIO PINAR FL Self Employed Mortgage LENDERSRIDGECREST FL Self Employed Mortgage LENDERSRESTON FL Self Employed Mortgage LENDERSREDLAND FL Self Employed Mortgage LENDERSRED HEAD FL Self Employed Mortgage LENDERSRAINBOW LAKES ESTATES FL Self Employed Mortgage LENDERSPINETTA FL Self Employed Mortgage LENDERSPINEOLA FL Self Employed Mortgage LENDERSPINECREST, HILLSBOROUGH COUNTY FL Self Employed Mortgage LENDERSPINE ISLAND, CALHOUN COUNTY FL Self Employed Mortgage LENDERSPICNIC FL Self Employed Mortgage LENDERSPETERS FL Self Employed Mortgage LENDERSPERDIDO KEY FL Self Employed Mortgage LENDERSPENSACOLA BEACH FL Self Employed Mortgage LENDERSPENNICHAW FL Self Employed Mortgage LENDERSPELICAN LAKE FL Self Employed Mortgage LENDERSPARRISH FL Self Employed Mortgage LENDERSPANACEA FL Self Employed Mortgage LENDERSPALMDALE FL Self Employed Mortgage LENDERSPALMA SOLA FL Self Employed Mortgage LENDERSPALM RIVER FL Self Employed Mortgage LENDERSPALM HARBOR FL Self Employed Mortgage LENDERSPALM BEACH FARMS FL Self Employed Mortgage LENDERSPAINTERS HILL FL Self Employed Mortgage LENDERSOZONA FL Self Employed Mortgage LENDERSOZELLO FL Self Employed Mortgage LENDERSOXFORD FL Self Employed Mortgage LENDERSOSTEEN FL Self Employed Mortgage LENDERSOSLO FL Self Employed Mortgage LENDERSORTONA, GLADES COUNTY FL Self Employed Mortgage LENDERSORLO VISTA FL Self Employed Mortgage LENDERSORIOLE BEACH FL Self Employed Mortgage LENDERSORIENT PARK FL Self Employed Mortgage LENDERSORANGE SPRINGS FL Self Employed Mortgage LENDERSORANGE LAKE FL Self Employed Mortgage LENDERSORANGE BEND FL Self Employed Mortgage LENDERSONECO FL Self Employed Mortgage LENDERSONA FL Self Employed Mortgage LENDERSOLUSTEE FL Self Employed Mortgage LENDERSOLD TOWN FL Self Employed Mortgage LENDERSOLD MYAKKA FL Self Employed Mortgage LENDERSOKEELANTA FL Self Employed Mortgage LENDERSOJUS FL Self Employed Mortgage LENDERSOCKLAWAHA FL Self Employed Mortgage LENDERSOCHOPEE FL Self Employed Mortgage LENDERSOCHLOCKONEE FL Self Employed Mortgage LENDERSOCHEESEULGA FL Self Employed Mortgage LENDERSOCHEESEE LANDING FL Self Employed Mortgage LENDERSOAK RIDGE FL Self Employed Mortgage LENDERSO’NEIL FL Self Employed Mortgage LENDERSO’BRIEN FL Self Employed Mortgage LENDERSNOWATNEY FL Self Employed Mortgage LENDERSNORTH RUSKIN FL Self Employed Mortgage LENDERSNORTH NAPLES FL Self Employed Mortgage LENDERSNORTH MEADOWBROOK TERRACE FL Self Employed Mortgage LENDERSNOCATEE, ST. JOHNS COUNTY FL Self Employed Mortgage LENDERSNOCATEE, DESOTO COUNTY FL Self Employed Mortgage LENDERSNICHOLS FL Self Employed Mortgage LENDERSNEWPORT, WAKULLA COUNTY FL Self Employed Mortgage LENDERSNEWPORT, MONROE COUNTY FL Self Employed Mortgage LENDERSNEW HOPE FL Self Employed Mortgage LENDERSNEALS FL Self Employed Mortgage LENDERSNAVARRE FL Self Employed Mortgage LENDERSNAVARRE BEACH FL Self Employed Mortgage LENDERSNASSAUVILLE FL Self Employed Mortgage LENDERSNARCOOSSEE FL Self Employed Mortgage LENDERSNALCREST FL Self Employed Mortgage LENDERSMYAKKA CITY FL Self Employed Mortgage LENDERSMUCE FL Self Employed Mortgage LENDERSMOUNTAIN LAKE FL Self Employed Mortgage LENDERSMOUNT PLEASANT FL Self Employed Mortgage LENDERSMONKEY BOX FL Self Employed Mortgage LENDERSMILLVILLE FL Self Employed Mortgage LENDERSMILLIGAN FL Self Employed Mortgage LENDERSMILES CITY FL Self Employed Mortgage LENDERSMIKESVILLE FL Self Employed Mortgage LENDERSMIDWAY, SANTA ROSA COUNTY FL Self Employed Mortgage LENDERSMICCOSUKEE FL Self Employed Mortgage LENDERSMERIDIAN FL Self Employed Mortgage LENDERSMELROSE FL Self Employed Mortgage LENDERSMELBOURNE SHORES FL Self Employed Mortgage LENDERSMEDART FL Self Employed Mortgage LENDERSMEADOWCREST FL Self Employed Mortgage LENDERSMEADOWBROOK TERRACE FL Self Employed Mortgage LENDERSMCRAE FL Self Employed Mortgage LENDERSMCNEAL FL Self Employed Mortgage LENDERSMCDAVID FL Self Employed Mortgage LENDERSMCALPIN FL Self Employed Mortgage LENDERSMAYTOWN FL Self Employed Mortgage LENDERSMARYSVILLE FL Self Employed Mortgage LENDERSMARTIN FL Self Employed Mortgage LENDERSMARION OAKS FL Self Employed Mortgage LENDERSMABEL FL Self Employed Mortgage LENDERSLULU FL Self Employed Mortgage LENDERSLUDLAM FL Self Employed Mortgage LENDERSLOXAHATCHEE FL Self Employed Mortgage LENDERSLOWELL FL Self Employed Mortgage LENDERSLOTTIEVILLE FL Self Employed Mortgage LENDERSLORIDA FL Self Employed Mortgage LENDERSLOCHLOOSA FL Self Employed Mortgage LENDERSLLOYD FL Self Employed Mortgage LENDERSLITTLE LAKE CITY FL Self Employed Mortgage LENDERSLITHIA FL Self Employed Mortgage LENDERSLINDEN FL Self Employed Mortgage LENDERSLILLIBRIDGE FL Self Employed Mortgage LENDERSLETO FL Self Employed Mortgage LENDERSLESSIE FL Self Employed Mortgage LENDERSLEONARDS FL Self Employed Mortgage LENDERSLEMON BLUFF FL Self Employed Mortgage LENDERSLANSING FL Self Employed Mortgage LENDERSLANIER FL Self Employed Mortgage LENDERSLANARK VILLAGE FL Self Employed Mortgage LENDERSLAMONT FL Self Employed Mortgage LENDERSLAKEWOOD FL Self Employed Mortgage LENDERSLAKEWOOD RANCH FL Self Employed Mortgage LENDERSLAKESHORE FL Self Employed Mortgage LENDERSLAKEPORT FL Self Employed Mortgage LENDERSLAKE TALLAVANA FL Self Employed Mortgage LENDERSLAKE SUZY FL Self Employed Mortgage LENDERSLAKE MONROE FL Self Employed Mortgage LENDERSLAKE MARY JANE FL Self Employed Mortgage LENDERSLAKE HART FL Self Employed Mortgage LENDERSLAKE GENEVA FL Self Employed Mortgage LENDERSLAKE FERN FL Self Employed Mortgage LENDERSLAKE COMO FL Self Employed Mortgage LENDERSLAKE BUTLER, ORANGE COUNTY FL Self Employed Mortgage LENDERSKORONA FL Self Employed Mortgage LENDERSKNIGHTS FL Self Employed Mortgage LENDERSKINGS FERRY FL Self Employed Mortgage LENDERSKINARD FL Self Employed Mortgage LENDERSKILLARNEY FL Self Employed Mortgage LENDERSKEYSVILLE FL Self Employed Mortgage LENDERSKEY HAVEN FL Self Employed Mortgage LENDERSKENT FL Self Employed Mortgage LENDERSKENDALL FL Self Employed Mortgage LENDERSKENDALL WEST FL Self Employed Mortgage LENDERSKENANSVILLE FL Self Employed Mortgage LENDERSKALAMAZOO FL Self Employed Mortgage LENDERSJULINGTON CREEK PLANTATION FL Self Employed Mortgage LENDERSJOSHUA FL Self Employed Mortgage LENDERSJONESVILLE FL Self Employed Mortgage LENDERSJEWFISH FL Self Employed Mortgage LENDERSJEROME FL Self Employed Mortgage LENDERSITALIA FL Self Employed Mortgage LENDERSISLEWORTH FL Self Employed Mortgage LENDERSISLANDIA FL Self Employed Mortgage LENDERSISLAND GROVE FL Self Employed Mortgage LENDERSIRVINE FL Self Employed Mortgage LENDERSIOLEE FL Self Employed Mortgage LENDERSINTERCESSION CITY FL Self Employed Mortgage LENDERSINNERARITY POINT FL Self Employed Mortgage LENDERSINGLE FL Self Employed Mortgage LENDERSINDIANOLA FL Self Employed Mortgage LENDERSINDIAN MOUND VILLAGE FL Self Employed Mortgage LENDERSINDIAN LAKE ESTATES FL Self Employed Mortgage LENDERSIAMONIA FL Self Employed Mortgage LENDERSHUNTINGTON, PUTNAM COUNTY FL Self Employed Mortgage LENDERSHUNTINGTON, MARION COUNTY FL Self Employed Mortgage LENDERSHUNTER’S CREEK FL Self Employed Mortgage LENDERSHULL FL Self Employed Mortgage LENDERSHUDSON BEACH FL Self Employed Mortgage LENDERSHOWARD FL Self Employed Mortgage LENDERSHOSFORD FL Self Employed Mortgage LENDERSHORIZON WEST FL Self Employed Mortgage LENDERSHOPEWELL, MADISON COUNTY FL Self Employed Mortgage LENDERSHOPEWELL, HILLSBOROUGH COUNTY FL Self Employed Mortgage LENDERSHOPEWELL GARDENS FL Self Employed Mortgage LENDERSHOMELAND FL Self Employed Mortgage LENDERSHOLT FL Self Employed Mortgage LENDERSHOLOPAW FL Self Employed Mortgage LENDERSHOLMES VALLEY FL Self Employed Mortgage LENDERSHOLLISTER FL Self Employed Mortgage LENDERSHOLDER FL Self Employed Mortgage LENDERSHOLDEN HEIGHTS FL Self Employed Mortgage LENDERSHINSON FL Self Employed Mortgage LENDERSHILLIARDVILLE FL Self Employed Mortgage LENDERSHIGHPOINT FL Self Employed Mortgage LENDERSHIGHLAND VIEW FL Self Employed Mortgage LENDERSHIGHLAND LAKES FL Self Employed Mortgage LENDERSHIBERNIA FL Self Employed Mortgage LENDERSHENDERSON MILL FL Self Employed Mortgage LENDERSHAWLEY HEIGHTS FL Self Employed Mortgage LENDERSHASAN FL Self Employed Mortgage LENDERSHARMONY FL Self Employed Mortgage LENDERSHARBOR BLUFFS FL Self Employed Mortgage LENDERSHAILE FL Self Employed Mortgage LENDERSHAILE PLANTATION FL Self Employed Mortgage LENDERSHAGUE FL Self Employed Mortgage LENDERSGULF HARBORS FL Self Employed Mortgage LENDERSGULF HAMMOCK FL Self Employed Mortgage LENDERSGREENHEAD FL Self Employed Mortgage LENDERSGREENBRIAR FL Self Employed Mortgage LENDERSGREEN-MAR ACRES FL Self Employed Mortgage LENDERSGRAYVIK FL Self Employed Mortgage LENDERSGRAYTON BEACH FL Self Employed Mortgage LENDERSGRANDIN FL Self Employed Mortgage LENDERSGRAND ISLAND FL Self Employed Mortgage LENDERSGRAHAM FL Self Employed Mortgage LENDERSGLENWOOD HEIGHTS FL Self Employed Mortgage LENDERSGIBSONIA FL Self Employed Mortgage LENDERSGEORGETOWN FL Self Employed Mortgage LENDERSGASKINS FL Self Employed Mortgage LENDERSGARDNER FL Self Employed Mortgage LENDERSGARDEN GROVE FL Self Employed Mortgage LENDERSGARDEN COVE FL Self Employed Mortgage LENDERSGANDY FL Self Employed Mortgage LENDERSFROG CITY FL Self Employed Mortgage LENDERSFRINK FL Self Employed Mortgage LENDERSFRANKLINTOWN FL Self Employed Mortgage LENDERSFOWLER’S BLUFF FL Self Employed Mortgage LENDERSFOUNTAIN FL Self Employed Mortgage LENDERSFORTYMILE BEND FL Self Employed Mortgage LENDERSFORT OGDEN FL Self Employed Mortgage LENDERSFORT MCCOY FL Self Employed Mortgage LENDERSFORT MASON FL Self Employed Mortgage LENDERSFORT FLORIDA FL Self Employed Mortgage LENDERSFORT BRADEN FL Self Employed Mortgage LENDERSFLORIDANA BEACH FL Self Employed Mortgage LENDERSFLORAHOME FL Self Employed Mortgage LENDERSFLEMING ISLAND FL Self Employed Mortgage LENDERSFLAGLER ESTATES FL Self Employed Mortgage LENDERSFIVE POINTS, WASHINGTON COUNTY FL Self Employed Mortgage LENDERSFISHER CORNER FL Self Employed Mortgage LENDERSFISH CREEK FL Self Employed Mortgage LENDERSFERN PARK FL Self Employed Mortgage LENDERSFERN CREST VILLAGE FL Self Employed Mortgage LENDERSFELLOWSHIP FL Self Employed Mortgage LENDERSFELKEL FL Self Employed Mortgage LENDERSFELDA FL Self Employed Mortgage LENDERSFEDERAL POINT FL Self Employed Mortgage LENDERSFEATHER SOUND FL Self Employed Mortgage LENDERSFAVORETTA FL Self Employed Mortgage LENDERSFARMTON FL Self Employed Mortgage LENDERSFANLEW FL Self Employed Mortgage LENDERSFALMOUTH FL Self Employed Mortgage LENDERSFAIRVILLA FL Self Employed Mortgage LENDERSFAIRVIEW SHORES FL Self Employed Mortgage LENDERSFAIRFIELD FL Self Employed Mortgage LENDERSEVINSTON FL Self Employed Mortgage LENDERSEVERGREEN FL Self Employed Mortgage LENDERSEUFALA FL Self Employed Mortgage LENDERSESTIFFANULGA FL Self Employed Mortgage LENDERSESPANOLA FL Self Employed Mortgage LENDERSESCAMBIA FARMS FL Self Employed Mortgage LENDERSENTERPRISE FL Self Employed Mortgage LENDERSEMPORIA FL Self Employed Mortgage LENDERSEMATHLA FL Self Employed Mortgage LENDERSELKTON FL Self Employed Mortgage LENDERSEL JOBEAN FL Self Employed Mortgage LENDERSEL CHICO FL Self Employed Mortgage LENDERSEGYPT LAKE FL Self Employed Mortgage LENDERSEDGEVILLE FL Self Employed Mortgage LENDERSEDGAR FL Self Employed Mortgage LENDERSEATON PARK FL Self Employed Mortgage LENDERSEAST TAMPA FL Self Employed Mortgage LENDERSEAST NAPLES FL Self Employed Mortgage LENDERSEAST LAKE, PINELLAS COUNTY FL Self Employed Mortgage LENDERSEAST LAKE, HILLSBOROUGH COUNTY FL Self Employed Mortgage LENDERSEAST LAKE WEIR FL Self Employed Mortgage LENDERSEARLETON FL Self Employed Mortgage LENDERSDYAL FL Self Employed Mortgage LENDERSDURANT FL Self Employed Mortgage LENDERSDUPONT FL Self Employed Mortgage LENDERSDUCK KEY FL Self Employed Mortgage LENDERSDRIFTON FL Self Employed Mortgage LENDERSDR. PHILLIPS FL Self Employed Mortgage LENDERSDOWLING PARK FL Self Employed Mortgage LENDERSDOGTOWN FL Self Employed Mortgage LENDERSDOCTORS INLET FL Self Employed Mortgage LENDERSDEL RIO FL Self Employed Mortgage LENDERSDEERLAND FL Self Employed Mortgage LENDERSDEERING BAY FL Self Employed Mortgage LENDERSDEER PARK FL Self Employed Mortgage LENDERSDEEP CREEK FL Self Employed Mortgage LENDERSDEEM CITY FL Self Employed Mortgage LENDERSDAYTONA NORTH FL Self Employed Mortgage LENDERSDAY FL Self Employed Mortgage LENDERSDALKEITH FL Self Employed Mortgage LENDERSDAHOMA FL Self Employed Mortgage LENDERSDAHLBERG FL Self Employed Mortgage LENDERSCYPRESS FL Self Employed Mortgage LENDERSCURTIS FL Self Employed Mortgage LENDERSCUDJOE KEY FL Self Employed Mortgage LENDERSCUBITIS FL Self Employed Mortgage LENDERSCRYSTAL BEACH FL Self Employed Mortgage LENDERSCROSS CREEK FL Self Employed Mortgage LENDERSCROOM-A-COOCHEE FL Self Employed Mortgage LENDERSCREIGHTON FL Self Employed Mortgage LENDERSCRAWFORDVILLE FL Self Employed Mortgage LENDERSCRAWFORD FL Self Employed Mortgage LENDERSCRAGGS FL Self Employed Mortgage LENDERSCOX FL Self Employed Mortgage LENDERSCOW CREEK FL Self Employed Mortgage LENDERSCOURTENAY FL Self Employed Mortgage LENDERSCOUNTRY CLUB FL Self Employed Mortgage LENDERSCORAL WAY VILLAGE FL Self Employed Mortgage LENDERSCORAL TERRACE FL Self Employed Mortgage LENDERSCOPELAND FL Self Employed Mortgage LENDERSCOOPERTOWN FL Self Employed Mortgage LENDERSCONWAY FL Self Employed Mortgage LENDERSCONCH KEY FL Self Employed Mortgage LENDERSCODY FL Self Employed Mortgage LENDERSCODY’S CORNER FL Self Employed Mortgage LENDERSCLAY HILL FL Self Employed Mortgage LENDERSCLARKSVILLE FL Self Employed Mortgage LENDERSCLARCONA FL Self Employed Mortgage LENDERSCLAIR-MEL CITY FL Self Employed Mortgage LENDERSCITRUS CENTER FL Self Employed Mortgage LENDERSCITRA FL Self Employed Mortgage LENDERSCHRISTMAS FL Self Employed Mortgage LENDERSCHATHAM FL Self Employed Mortgage LENDERSCHASON FL Self Employed Mortgage LENDERSCHARLOTTE HARBOR FL Self Employed Mortgage LENDERSCHAIRES FL Self Employed Mortgage LENDERSCENTERVILLE FL Self Employed Mortgage LENDERSCASSADAGA FL Self Employed Mortgage LENDERSCARROLLWOOD FL Self Employed Mortgage LENDERSCARROLLWOOD VILLAGE FL Self Employed Mortgage LENDERSCARNESTOWN FL Self Employed Mortgage LENDERSCAPPS FL Self Employed Mortgage LENDERSCAPITOLA FL Self Employed Mortgage LENDERSCAPE SAN BLAS FL Self Employed Mortgage LENDERSCANDLER FL Self Employed Mortgage LENDERSCANAVERAL GROVES FL Self Employed Mortgage LENDERSBULL CREEK FL Self Employed Mortgage LENDERSBRYCEVILLE FL Self Employed Mortgage LENDERSBRYANT FL Self Employed Mortgage LENDERSBOARDMAN FL Self Employed Mortgage LENDERSBROWNVILLE FL Self Employed Mortgage LENDERSBROWNSVILLE FL Self Employed Mortgage LENDERSBROWNSVILLE, ESCAMBIA COUNTY FL Self Employed Mortgage LENDERSBROAD BRANCH FL Self Employed Mortgage LENDERSBRADLEY JUNCTION FL Self Employed Mortgage LENDERSBRADFORDVILLE FL Self Employed Mortgage LENDERSBOYETTE FL Self Employed Mortgage LENDERSBOULOGNE FL Self Employed Mortgage LENDERSBOSTWICK FL Self Employed Mortgage LENDERSBODEN FL Self Employed Mortgage LENDERSBOCA WEST FL Self Employed Mortgage LENDERSBOCA GRANDE FL Self Employed Mortgage LENDERSBITHLO FL Self Employed Mortgage LENDERSBISCAYNE GARDENS FL Self Employed Mortgage LENDERSBIMINI FL Self Employed Mortgage LENDERSBIG PINE KEY FL Self Employed Mortgage LENDERSBIG COPPITT KEY FL Self Employed Mortgage LENDERSBETHUNE BEACH FL Self Employed Mortgage LENDERSBETHLEHEM FL Self Employed Mortgage LENDERSBENSON JUNCTION FL Self Employed Mortgage LENDERSBELLAIR, CLAY COUNTY FL Self Employed Mortgage LENDERSBELAIR, LEON COUNTY FL Self Employed Mortgage LENDERSBECKER FL Self Employed Mortgage LENDERSBEAR CREEK FL Self Employed Mortgage LENDERSBEALSVILLE FL Self Employed Mortgage LENDERSBAYOU GEORGE FL Self Employed Mortgage LENDERSBAY POINT, MONROE COUNTY FL Self Employed Mortgage LENDERSBAY PINES FL Self Employed Mortgage LENDERSBAY CREST PARK FL Self Employed Mortgage LENDERSBARRINEAU PARK FL Self Employed Mortgage LENDERSBAREFOOT BAY FL Self Employed Mortgage LENDERSBARDMOOR FL Self Employed Mortgage LENDERSBARDIN FL Self Employed Mortgage LENDERSBARBERVILLE FL Self Employed Mortgage LENDERSBARBER QUARTERS FL Self Employed Mortgage LENDERSBANANA FL Self Employed Mortgage LENDERSBALD POINT FL Self Employed Mortgage LENDERSBAKER FL Self Employed Mortgage LENDERSAZALEA PARK FL Self Employed Mortgage LENDERSAURANTIA FL Self Employed Mortgage LENDERSAUCILLA FL Self Employed Mortgage LENDERSARMSTRONG FL Self Employed Mortgage LENDERSARIPEKA FL Self Employed Mortgage LENDERSARGYLE FL Self Employed Mortgage LENDERSANTIOCH FL Self Employed Mortgage LENDERSANTHONY FL Self Employed Mortgage LENDERSANGLERS PARK FL Self Employed Mortgage LENDERSAMERICAN BEACH FL Self Employed Mortgage LENDERSAMELIA CITY FL Self Employed Mortgage LENDERSALTURAS FL Self Employed Mortgage LENDERSALTON FL Self Employed Mortgage LENDERSALLIGATOR POINT FL Self Employed Mortgage LENDERSALLANDALE FL Self Employed Mortgage LENDERSALAMANA FL Self Employed Mortgage LENDERSALAFAYA FL Self Employed Mortgage LENDERSADAMSVILLE, SUMTER COUNTY FL Self Employed Mortgage LENDERSADAMSVILLE, HILLSBOROUGH COUNTY FL Self Employed Mortgage LENDERSTHE ACREAGE FL Self Employed Mortgage LENDERSABE SPRINGS FL Self Employed Mortgage LENDERSWINTER SPRINGS FL Self Employed Mortgage LENDERSWINTER PARK FL Self Employed Mortgage LENDERSWINTER HAVEN FL Self Employed Mortgage LENDERSWINTER GARDEN FL Self Employed Mortgage LENDERSWILTON MANORS FL Self Employed Mortgage LENDERSWESTON FL Self Employed Mortgage LENDERSWEST PALM BEACH FL Self Employed Mortgage LENDERSWEST MELBOURNE FL Self Employed Mortgage LENDERSWELLINGTON FL Self Employed Mortgage LENDERSVERO BEACH FL Self Employed Mortgage LENDERSVENICE FL Self Employed Mortgage LENDERSVALPARAISO FL Self Employed Mortgage LENDERSTREASURE ISLAND FL Self Employed Mortgage LENDERSTITUSVILLE FL Self Employed Mortgage LENDERSTEMPLE TERRACE FL Self Employed Mortgage LENDERSTAVARES FL Self Employed Mortgage LENDERSTARPON SPRINGS FL Self Employed Mortgage LENDERSTAMPA FL Self Employed Mortgage LENDERSTAMARAC FL Self Employed Mortgage LENDERSTALLAHASSEE FL Self Employed Mortgage LENDERSSURFSIDE FL Self Employed Mortgage LENDERSSTUART FL Self Employed Mortgage LENDERSSEWALL’S POINT FL Self Employed Mortgage LENDERSSHALIMAR FL Self Employed Mortgage LENDERSSEBASTIAN FL Self Employed Mortgage LENDERSSEASIDE FL Self Employed Mortgage LENDERSSATELLITE BEACH FL Self Employed Mortgage LENDERSSARASOTA FL Self Employed Mortgage LENDERSSANIBEL FL Self Employed Mortgage LENDERSSANFORD FL Self Employed Mortgage LENDERSSAFETY HARBOR FL Self Employed Mortgage LENDERSST. PETERSBURG FL Self Employed Mortgage LENDERSST. PETE BEACH FL Self Employed Mortgage LENDERS ST. CLOUD FL Self Employed Mortgage LENDERSST. AUGUSTINE BEACH FL Self Employed Mortgage LENDERSST. AUGUSTINE FL Self Employed Mortgage LENDERS ROYAL PALM BEACH FL Self Employed Mortgage LENDERSROCKLEDGE FL Self Employed Mortgage LENDERSPUNTA GORDA FL Self Employed Mortgage LENDERSPORT ST. LUCIE FL Self Employed Mortgage LENDERSPORT ORANGE FL Self Employed Mortgage LENDERSPONCE INLET FL Self Employed Mortgage LENDERSPOMPANO BEACH FL Self Employed Mortgage LENDERSPLANTATION FL Self Employed Mortgage LENDERSPLANT CITY FL Self Employed Mortgage LENDERSPINELLAS PARK FL Self Employed Mortgage LENDERSPINECREST FL Self Employed Mortgage LENDERSPENSACOLA FL Self Employed Mortgage LENDERSPEMBROKE PINES FL Self Employed Mortgage LENDERSPANAMA CITY BEACH FL Self Employed Mortgage LENDERSPANAMA CITY FL Self Employed Mortgage LENDERSPALMETTO FL Self Employed Mortgage LENDERSPALM COAST FL Self Employed Mortgage LENDERSPALM BEACH GARDENS FL Self Employed Mortgage LENDERSPALM BEACH FL Self Employed Mortgage LENDERSPALM BAY FL Self Employed Mortgage LENDERSPALATKA FL Self Employed Mortgage LENDERSOVIEDO FL Self Employed Mortgage LENDERSORMOND BEACH FL Self Employed Mortgage LENDERSORLANDO FL Self Employed Mortgage LENDERSORANGE PARK FL Self Employed Mortgage LENDERSOLDSMAR FL Self Employed Mortgage LENDERSOKEECHOBEE FL Self Employed Mortgage LENDERSOCOEE FL Self Employed Mortgage LENDERSOCEAN RIDGE FL Self Employed Mortgage LENDERSOCALA FL Self Employed Mortgage LENDERSOAKLAND PARK FL Self Employed Mortgage LENDERSNORTH PORT FL Self Employed Mortgage LENDERSNORTH MIAMI BEACH FL Self Employed Mortgage LENDERSNORTH MIAMI FL Self Employed Mortgage LENDERSNICEVILLE FL Self Employed Mortgage LENDERSNEW SMYRNA BEACH FL Self Employed Mortgage LENDERSNEW PORT RICHEY FL Self Employed Mortgage LENDERSNEPTUNE BEACH FL Self Employed Mortgage LENDERSNAPLES FL Self Employed Mortgage LENDERSMOUNT DORA FL Self Employed Mortgage LENDERSMIRAMAR FL Self Employed Mortgage LENDERS-MIN 580 CREDITMINNEOLA FL Self Employed Mortgage LENDERSMILTON FL Self Employed Mortgage LENDERSMIAMI BEACH FL Self Employed Mortgage LENDERSMIAMI FL Self Employed Mortgage LENDERSMELBOURNE BEACH FL Self Employed Mortgage LENDERSMELBOURNE FL Self Employed Mortgage LENDERSMARGATE FL Self Employed Mortgage LENDERSMARCO ISLAND FL Self Employed Mortgage LENDERSMAITLAND FL Self Employed Mortgage LENDERSLONGWOOD FL Self Employed Mortgage LENDERSLONGBOAT KEY FL Self Employed Mortgage LENDERSLIGHTHOUSE POINT FL Self Employed Mortgage LENDERSLEESBURG FL Self Employed Mortgage LENDERSLAUDERHILL FL Self Employed Mortgage LENDERSLAUDERDALE BY THE SEA FL Self Employed Mortgage LENDERSLARGO FL Self Employed Mortgage LENDERSLANTANA FL Self Employed Mortgage LENDERSLAKE WORTH FL Self Employed Mortgage LENDERSLAKE WALES FL Self Employed Mortgage LENDERSLAKE PARK FL Self Employed Mortgage LENDERSLAKE MARY FL Self Employed Mortgage LENDERSLAKELAND FL Self Employed Mortgage LENDERSLAKE ALFRED FL Self Employed Mortgage LENDERSLADY LAKE FL Self Employed Mortgage LENDERSLABELLE FL Self Employed Mortgage LENDERSKISSIMMEE FL Self Employed Mortgage LENDERSKEY WEST FL Self Employed Mortgage LENDERSKEY BISCAYNE FL Self Employed Mortgage LENDERSJUPITER FL Self Employed Mortgage LENDERSJUNO BEACH FL Self Employed Mortgage LENDERSJACKSONVILLE FL Self Employed Mortgage LENDERSINDIALANTIC FL Self Employed Mortgage LENDERSHYPOLUXO FL Self Employed Mortgage LENDERSHOMESTEAD FL Self Employed Mortgage LENDERSHOLMES BEACH FL Self Employed Mortgage LENDERSHOLLY HILL FL Self Employed Mortgage LENDERSHOLLYWOOD FL Self Employed Mortgage LENDERSHIGHLAND BEACH FL Self Employed Mortgage LENDERSHIALEAH GARDENS FL Self Employed Mortgage LENDERSHIALEAH FL Self Employed Mortgage LENDERSHAWTHORNE FL Self Employed Mortgage LENDERSHALLANDALE BEACH FL Self Employed Mortgage LENDERSHAINES CITY FL Self Employed Mortgage LENDERSGULFPORT FL Self Employed Mortgage LENDERSGULF BREEZE FL Self Employed Mortgage LENDERSGREEN COVE SPRINGS FL Self Employed Mortgage LENDERSGREENACRES FL Self Employed Mortgage LENDERSGAINESVILLE FL Self Employed Mortgage LENDERSFRUITLAND PARK FL Self Employed Mortgage LENDERSFORT WALTON BEACH FL Self Employed Mortgage LENDERSFORT PIERCE FL Self Employed Mortgage LENDERSFORT MYERS BEACH FL Self Employed Mortgage LENDERSFORT MYERS FL Self Employed Mortgage LENDERSFORT MEADE FL Self Employed Mortgage LENDERSFORT LAUDERDALE FL Self Employed Mortgage LENDERSEUSTIS FL Self Employed Mortgage LENDERSEDGEWOOD FL Self Employed Mortgage LENDERSEDGEWATER FL Self Employed Mortgage LENDERSEAGLE LAKE FL Self Employed Mortgage LENDERSDUNEDIN FL Self Employed Mortgage LENDERSDESTIN FL Self Employed Mortgage LENDERSDELTONA FL Self Employed Mortgage LENDERSDELRAY BEACH FL Self Employed Mortgage LENDERSDELAND FL Self Employed Mortgage LENDERSDEFUNIAK SPRINGS FL Self Employed Mortgage LENDERSDEERFIELD BEACH FL Self Employed Mortgage LENDERSDAYTONA BEACH FL Self Employed Mortgage LENDERSDAVIE FL Self Employed Mortgage LENDERSDANIA BEACH FL Self Employed Mortgage LENDERSCRYSTAL RIVER FL Self Employed Mortgage LENDERSCORAL SPRINGS FL Self Employed Mortgage LENDERSCORAL GABLES FL Self Employed Mortgage LENDERSCOCONUT CREEK FL Self Employed Mortgage LENDERSCOCOA BEACH FL Self Employed Mortgage LENDERS