GEORGIA CO-OP MORTGAGE LENDERS

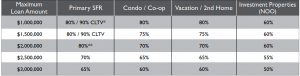

GEORGIA CO-OP MORTGAGE LENDERS LOAN TO VALUE

GEORGIA CO-OP MORTGAGE LENDERS TERMS

The ARM is a 1st mortgage adjustable rate loan with principal and interest payments amortized over 30 years.

- 3/1 ARM: Rate is fixed for 3 years.

- 5/1 ARM: Rate is fixed for 5 years.

- 7/1 ARM: Rate is fixed for 7 years.

- 30 Year fixed for 30 years.

GEORGIA CO-OP MINIMUM & MAX LOAN AMOUNTS

• $100,000 minimum loan amount. Exceptions considered on a case-by-case.

• Co0OP Loan amount exceptions over $4,000,000 available.

GEORGIA CO-OP MORTGAGE LENDERS CREDIT REQUIREMENTS

• 680 middle score required with some exceptions allowed for lack of credit or unestablished credit.

• For co-co-op mortgage applicants and co-mortgagers, the lowest mid-score is used for pricing and qualification.

• Meeting the minimum credit score requirement does not automatically constitute a credit approval. A pattern of

adverse credit or overextended credit may disqualify co-op mortgage applicant from financing, even if the minimum credit score is met.

• Credit report is used for Pre-Approval and co-op mortgage lenders will also pull credit before issuing a conditional

approval. Mid-score from co-op mortgage lenders credit pull is used for pricing and qualification.

No Credit or Limited Credit

• No credit or limited credit profiles are allowed on a case-by-case basis for U.S. citizens.

• No U.S. credit or credit score is required for the Work Visa/Expatriate/Immigrant Program or Foreign National Program

GEORGIA CO-OP MORTGAGE LENDERS OPTIONS INCLUDE:

- Primary GEORGIA Co-op Mortgage Lenders

- Second Home GEORGIA Co-op Mortgage Lenders

- Investments GEORGIA Co-op Mortgage Lenders

- Cash Out GEORGIA Co-op Refinancing

- Second GEORGIA Co-op Home Financing

- Jumbo GEORGIA Co-op Loans

- Low GEORGIA Co-op Closing Costs

- Up to 80 Percent GEORGIA Co-op Mortgage Loans

GEORGIA CO-OP MORTGAGE MAXIMUM DEBT TO INCOME

Maximum GEORGIA CO-op Mortgage Lenders Debt To Income Ratio

• 43% maximum back-end ratio.

GEORGIA CO-OP MORTGAGE LENDERS APPROVAL PROCESS

2. PRINT OUT CONDO QUESTIONNAIRE FOR ASSOCIATION TO FILL OUT COMPLETE. the questionnaire must be 100% complete for Approval Commitment. No blanks or questions answered “n/a”

or “unknown,” and the questionnaire must pass underwriter review.

ELIGIBLE GEORGIA CO-OP PROPERTY TYPES & OCCUPANCY

GEORGIA Co-op Occupancy Permitted

• Primary GEORGIA Co-op Residence

• Second GEORGIA Co-op Home (minimal rental income allowed)

• Investment GEORGIA Co-op Property (non-owner GEORGIA Co-op occupied) permitted at maximum GEORGIA Co-op loan of 60% LTV

ELIGIBLE GEORGIA CO-OP MORTGAGE REQUIREMENTS

• Minimum Down Payment 20% For GEORGIA Co-op Mortgage Lenders

• Title Insurance for GEORGIA Co-ops title policy issued through a title company or closing attorney must be issued on GEORGIA Co-op certificate

• Leaseholds GEORGIA Co-op allowed on a case-by-case basis

BAD CREDIT GEORGIA CO-OP MORTGAGE LENDERS CREDIT REQUIREMENTS

• Late payments on any mortgage, installment or revolving account of 2×30, 1×60 or more will typically disqualify a

borrower from financing. Exceptions will be reviewed on a case-by-case basis at a lower LTV.

• A pattern of adverse credit or overextended credit may disqualify borrower from financing, even if minimum credit score

is met. Borrowers with 3x monthly income amount in unsecured consumer debt are generally disqualified.

GEORGIA CO-OP MORTGAGE LENDERS REQUIREMENTS AFTER FORECLOSURE, BANKRUPTCY, SHORT SALE

• (4)Four-year seasoning from BK discharge date or sale of property

• Maximum 60% LTV or 40% downpayment

• No derogatory credit allowed since the bad credit event

• Strong extenuating circumstance and signed letter of explanation from co-op mortgage applicant detailing event required.

NOT ALLOWABLE FOR GEORGIA CO-OP MORTGAGE LENDERS

– Structural GEORGIA Co-op deficiencies and certain pending litigation (please contact your AE if litigation is not related to a structural issue)

– Incomplete GEORGIA Co-op construction of the subject phase

APPROVED OR ALLOWED GEORGIA CO-OP MORTGAGE LENDERS CASE BY CASE:

– Low GEORGIA Co-op HOA budget reserves

– HOA GEORGIA Co-op delinquencies exceeding 15%

• GEORGIA Co-op mortgage lenders Questionnaire must be 100% complete for Approval Commitment. No blanks or questions answered “n/a” or “unknown,” and the GEORGIA Co-op questionnaire must pass underwriter review.

• GEORGIA Co-ops mortgage lenders price GEORGIA Co-ops the same as Non-Warrantable Condos, regardless of loan size or GEORGIA Co-op questionnaire findings.

• GEORGIA Co-op must pust have a full kitchen and at least one separate bedroom. Minimum GEORGIA Co-op size 500 square feet generally required. Efficiency GEORGIA Co-ops or studio units are not permitted.

• Coinsurance GEORGIA Co-op is considered case-by-case if no agreed amount endorsement is available.

SELF EMPLOYED GEORGIA CO-OP MORTGAGE LENDERS

Self-Employed co-op mortgage Income calculations

• Borrower should be self-employed in the U.S. for a minimum of 2 years (max 80% LTV).

• 2-years business & personal tax returns required, plus year-to-date Profit & Loss statement.

• Business tax returns required for all businesses in which the borrower has 25% ownership or more. On occasion

business tax returns are needed if the borrower is has less than 25% ownership.

• Fannie Mae cash flow analysis form can be used.

• NOL Carryover Loss: Treated case-by-case when truly a one-time occurrence (i.e. real estate loss, lawsuit settlement or some other form of a truly one-time occurrence). Detailed CPA letter addressing the one-time occurrence is required.

• Less than two years self-employment is considered on a case-by-case basis with a reduced LTV.

REQUIRED BY GEORGIA CO-OP MORTGAGE LENDERS

• 2-months bank statements for monthly asset accounts, and most recent statement for quarterly asset accounts

(VOD not permitted).

• 6 months PITI for all GEORGIA co-op properties owned including subject.

• At least 3 months of the subject property’s reserves must be liquid non-retirement.

GEORGIA CO-OP MORTGAGE LENDERS CASE BY CASE MORTGAGE APPROVALS

• GEORGIA Co-op Current reserve balance meets or exceeds 2 months of the subject property’s GEORGIA Co-op HOA dues in reserves multiplied by all GEORGIA Co-op units in the GEORGIA Co-op project or 10% or more reserve allocation designated in the most recent GEORGIA Co-op budget.

SECOND HOME GEORGIA CO-OP MORTGAGE LENDERS

• GEORGIA Co-op Mortgage Lenders will typically define a property as a second GEORGIA Co-op home if it is (1) located in a vacation or resort area 30 or more miles from the primary GEORGIA Co-op residence or (2) used a GEORGIA Co-op college housing for enrolled dependent within 5 miles of campus)

• Short-term GEORGIA Co-op rental income is allowed on second GEORGIA Co-op homes and generally does not constitute a GEORGIA Co-op investment property designation. GEORGIA Co-op Rental income cannot be used to qualify. An evaluation of the 1040 Schedule E is required.

GEORGIA CO-OP MORTGAGE FOR INVESTMENT PROPERTY

• Property titled in LLC allowed

• Maximum GEORGIA Co-op 60% LTV for investor GEORGIA Co-op mortgage lenders.

• Gross rental income is calculated by using a 12 month average of the net Schedule E income (Line 21) plus depreciation, mortgage interest paid to banks, taxes and insurance, and GEORGIA Co-op HOA dues.

• Rental income not appearing on Schedule E may be considered case-by-case with 3 months canceled checks and a

current lease agreement. Use 75% of gross rent as gross rental income.

• Immediate GEORGIA Co-op rental income on the purchase of an investment property is allowed using 75% of the monthly rent schedule as documented by Form 1007 or 1025.

• Cash-out is allowed up to $3,000,000 with no seasoning required.

WHAT IS A GEORGIA CO-OP AND HOW DO I GET A GEORGIA MORTGAGE?

A GEORGIA Co-op or cooperative apartment is an individual living unit within a GEORGIA Co-op building or development where a buyer purchases shares (equal to the value of the unit) in a GEORGIA Co-op corporation that holds title to a building Coops are predominantly located. Normally a GEORGIA Co-op sponsor will buy the building (takes out the underlying GEORGIA Co-op mortgage) and then will sell off the shares. Therefore, when buying a coop, you are actually buying GEORGIA Co-op shares in a corporation, not buying real property.

HOW TO GEORGIA CO-OP BUILDINGS GET PRE QUALIFIED BY GEORGIA MORTGAGE LENDERS?

To start with GEORGIA Co-op lender will look at the following factors to see if a particular GEORGIA Co-op building corresponds with their guidelines: the GEORGIA Co-op property’s resale value, investor concentration, and GEORGIA Co-op owner occupancy. Based on the previous example, if there are 20 units, five sponsor rentals and 15 sold units (with 12 owner-occupied units and 3 units being rented by the GEORGIA Co-op owners), the following ratios and guideline percentages result:

HOW IS A GEORGIA CO OP DIFFERENT FROM A HOUSE OR CONDO?

When you get a mortgage to purchase a house or condo you get the deed. But not with a GEORGIA Co-op, individual units do not have individual deeds. A GEORGIA Co-op mortgage is actually a “share-loan” or a loan that purchases a share within in the GEORGIA Co-op. The difference makes securing a loan for a GEORGIA Co-op more complicated them getting a traditional mortgage and fewer mortgage lenders offer share loans.

GEORGIA COOP BOARDS AND APPROVAL RULES

To buy into a GEORGIA Co-op, you must be approved by the GEORGIA Co-op board. The approval process is often extensive and may require interviews and character references, in addition to your employment, financial, and credit history. GEORGIA Co-op boards can refuse a prospective buyer for any reason, so long as it doesn’t run afoul of anti-discrimination policies. What you can do WITH your GEORGIA Co-op unit. As a GEORGIA Co-op shareholder, you don’t have the right of alienation where basically, you can’t sell your GEORGIA Co-op share (or rent your GEORGIA Co-op unit) without the permission of the GEORGIA Co-op board. Some GEORGIA Co-op associations have the right of first refusal, meaning they have the option to buy the property before you offer your GEORGIA Co-op to outside buyers. GEORGIA Co-op boards, though, can simply deny a sale without matching the sale price.

HOW GEORGIA COOP OWNERSHIP DIFFERS FROM CONDO OWNERSHIP

When you purchase a condominium you are purchasing a specific unit the surface and the interior walls of the unit in the space the condo contains. With a Co-op, you are purchasing a share in a corporation, which then entitles you to a unit. This share is considered personal property rather than real estate.

Co-Op Resources

- Buying into a Housing Cooperative

- Lessons for Success

- Resident Retention

- Starting a new Cooperative

- Benefits to Continuing as a Cooperative

- Pros & Cons to Owning a Cooperative

- What is a GEORGIA housing cooperative?

- What do I actually own?

- What does the share or membership purchase price involve?

- Do I pay real estate taxes?

- Are cooperatives allowed to discriminate?

- What do cooperatives look like?

- How to find a cooperative?

- What questions should I ask before buying into a cooperative?

- Economic Advantages

- Social Advantages

- Physical Benefits

- Standard Cooperative Practices

- What is a share loan?

- How do I accumulate equity?

- Market-rate housing cooperatives

- Limited-equity housing cooperatives

- Leasing cooperatives (or zero-equity)

- What are the monthly charges for?

GEORGIA CO-OP MORTGAGE LENDERS

- ABBEVILLE GEORGIA CO-OP MORTGAGE LENDERS

- ACWORTH GEORGIA CO-OP MORTGAGE LENDERS

- ADAIRSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- ADEL GEORGIA CO-OP MORTGAGE LENDERS

- ADRIAN GEORGIA CO-OP MORTGAGE LENDERS

- AILEY GEORGIA CO-OP MORTGAGE LENDERS

- ALAMO GEORGIA CO-OP MORTGAGE LENDERS

- ALAPAHA GEORGIA CO-OP MORTGAGE LENDERS

- ALBANY GEORGIA CO-OP MORTGAGE LENDERS

- ALDORA GEORGIA CO-OP MORTGAGE LENDERS

- ALLENHURST GEORGIA CO-OP MORTGAGE LENDERS

- ALLENTOWN GEORGIA CO-OP MORTGAGE LENDERS

- ALMA GEORGIA CO-OP MORTGAGE LENDERS

- ALPHARETTA GEORGIA CO-OP MORTGAGE LENDERS

- ALSTON GEORGIA CO-OP MORTGAGE LENDERS

- ALTO GEORGIA CO-OP MORTGAGE LENDERS

- AMBROSE GEORGIA CO-OP MORTGAGE LENDERS

- AMERICUS GEORGIA CO-OP MORTGAGE LENDERS

- ANDERSONVILLE GEORGIA CO-OP MORTGAGE LENDERS

- ARABI GEORGIA CO-OP MORTGAGE LENDERS

- ARAGON GEORGIA CO-OP MORTGAGE LENDERS

- ARCADE GEORGIA CO-OP MORTGAGE LENDERS

- ARGYLE GEORGIA CO-OP MORTGAGE LENDERS

- ARLINGTON GEORGIA CO-OP MORTGAGE LENDERS

- ASHBURN GEORGIA CO-OP MORTGAGE LENDERS

- ATHENS GEORGIA CO-OP MORTGAGE LENDERS

- ATLANTA GEORGIA CO-OP MORTGAGE LENDERS

- ATTAPULGUS GEORGIA CO-OP MORTGAGE LENDERS

- AUBURN GEORGIA CO-OP MORTGAGE LENDERS

- AUGUSTA GEORGIA CO-OP MORTGAGE LENDERS

- AUSTELL GEORGIA CO-OP MORTGAGE LENDERS

- AVERA GEORGIA CO-OP MORTGAGE LENDERS

- AVONDALE ESTATES GEORGIA CO-OP MORTGAGE LENDER

- BACONTON GEORGIA CO-OP MORTGAGE LENDERS

- BAINBRIDGE GEORGIA CO-OP MORTGAGE LENDERS

- BALDWIN GEORGIA CO-OP MORTGAGE LENDERS

- BALL GROUND GEORGIA CO-OP MORTGAGE LENDERS

- BARNESVILLE GEORGIA CO-OP MORTGAGE LENDERS

- BARTOW GEORGIA CO-OP MORTGAGE LENDERS

- BARWICK GEORGIA CO-OP MORTGAGE LENDERS

- BAXLEY GEORGIA CO-OP MORTGAGE LENDERS

- BERKELEY LAKE GEORGIA CO-OP MORTGAGE LENDERS

- BERLIN GEORGIA CO-OP MORTGAGE LENDERS

- BETHLEHEM GEORGIA CO-OP MORTGAGE LENDERS

- BISHOP GEORGIA CO-OP MORTGAGE LENDERS

- BLACKSHEAR GEORGIA CO-OP MORTGAGE LENDERS

- BLAIRSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- BLAKELY GEORGIA CO-OP MORTGAGE LENDERS

- BLOOMINGDALE GEORGIA CO-OP MORTGAGE LENDERS

- BLUE RIDGE GEORGIA CO-OP MORTGAGE LENDERS

- BLUFFTON GEORGIA CO-OP MORTGAGE LENDERS

- BLYTHE GEORGIA CO-OP MORTGAGE LENDERS

- BOGART GEORGIA CO-OP MORTGAGE LENDERS

- BOSTON GEORGIA CO-OP MORTGAGE LENDERS

- BOSTWICK GEORGIA CO-OP MORTGAGE LENDERS

- BOWDON GEORGIA CO-OP MORTGAGE LENDERS

- BOWERSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- BOWMAN GEORGIA CO-OP MORTGAGE LENDERS

- BRASELTON GEORGIA CO-OP MORTGAGE LENDERS

- BRASWELL GEORGIA CO-OP MORTGAGE LENDERS

- BREMEN GEORGIA CO-OP MORTGAGE LENDERS

- BRINSON GEORGIA CO-OP MORTGAGE LENDERS

- BRONWOOD GEORGIA CO-OP MORTGAGE LENDERS

- BROOKHAVEN GEORGIA CO-OP MORTGAGE LENDERS

- BROOKLET GEORGIA CO-OP MORTGAGE LENDERS

- BROOKS GEORGIA CO-OP MORTGAGE LENDERS

- BROXTON GEORGIA CO-OP MORTGAGE LENDERS

- BRUNSWICK GEORGIA CO-OP MORTGAGE LENDERS

- BUCHANAN GEORGIA CO-OP MORTGAGE LENDERS

- BUCKHEAD GEORGIA CO-OP MORTGAGE LENDERS

- BUENA VISTA GEORGIA CO-OP MORTGAGE LENDERS

- BUFORD GEORGIA CO-OP MORTGAGE LENDERS

- BUTLER GEORGIA CO-OP MORTGAGE LENDERS

- BYROMVILLE GEORGIA CO-OP MORTGAGE LENDERS

- BYRON GEORGIA CO-OP MORTGAGE LENDERS

- CADWELL GEORGIA CO-OP MORTGAGE LENDERS

- CAIRO GEORGIA CO-OP MORTGAGE LENDERS

- CALHOUN GEORGIA CO-OP MORTGAGE LENDERS

- CAMAK GEORGIA CO-OP MORTGAGE LENDERS

- CAMILLA GEORGIA CO-OP MORTGAGE LENDERS

- CANON GEORGIA CO-OP MORTGAGE LENDERS

- CANTON GEORGIA CO-OP MORTGAGE LENDERS

- CARL GEORGIA CO-OP MORTGAGE LENDERS

- CARLTON GEORGIA CO-OP MORTGAGE LENDERS

- CARNESVILLE GEORGIA CO-OP MORTGAGE LENDERS

- CARROLLTON GEORGIA CO-OP MORTGAGE LENDERS

- CARTERSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- CAVE SPRING GEORGIA CO-OP MORTGAGE LENDERS

- CECIL GEORGIA CO-OP MORTGAGE LENDERS

- CEDARTOWN GEORGIA CO-OP MORTGAGE LENDERS

- CENTERVILLE GEORGIA CO-OP MORTGAGE LENDERS

- CENTRALHATCHEE GEORGIA CO-OP MORTGAGE LENDERS

- CHAMBLEE GEORGIA CO-OP MORTGAGE LENDERS

- CHATSWORTH GEORGIA CO-OP MORTGAGE LENDERS

- CHATTAHOOCHEE HILLS GEORGIA CO-OP MORTGAGE LENDERS

- CHAUNCEY GEORGIA CO-OP MORTGAGE LENDERS

- CHESTER GEORGIA CO-OP MORTGAGE LENDERS

- CHICKAMAUGA GEORGIA CO-OP MORTGAGE LENDERS

- CLARKESVILLE GEORGIA CO-OP MORTGAGE LENDERS

- CLARKSTON GEORGIA CO-OP MORTGAGE LENDERS

- CLAXTON GEORGIA CO-OP MORTGAGE LENDERS

- CLAYTON GEORGIA CO-OP MORTGAGE LENDERS

- CLERMONT GEORGIA CO-OP MORTGAGE LENDERS

- CLEVELAND GEORGIA CO-OP MORTGAGE LENDERS

- CLIMAX GEORGIA CO-OP MORTGAGE LENDERS

- COBBTOWN GEORGIA CO-OP MORTGAGE LENDERS

- COCHRAN GEORGIA CO-OP MORTGAGE LENDERS

- COHUTTA GEORGIA CO-OP MORTGAGE LENDERS

- COLBERT GEORGIA CO-OP MORTGAGE LENDERS

- COLLEGE PARK GEORGIA CO-OP MORTGAGE LENDERS

- COLLINS GEORGIA CO-OP MORTGAGE LENDERS

- COLQUITT GEORGIA CO-OP MORTGAGE LENDERS

- COLUMBUS GEORGIA CO-OP MORTGAGE LENDERS

- COMER GEORGIA CO-OP MORTGAGE LENDERS

- COMMERCE GEORGIA CO-OP MORTGAGE LENDERS

- CONCORD GEORGIA CO-OP MORTGAGE LENDERS

- CONYERS GEORGIA CO-OP MORTGAGE LENDERS

- COOLIDGE GEORGIA CO-OP MORTGAGE LENDERS

- CORDELE GEORGIA CO-OP MORTGAGE LENDERS

- CORNELIA GEORGIA CO-OP MORTGAGE LENDERS

- COVINGTON GEORGIA CO-OP MORTGAGE LENDERS

- CRAWFORD GEORGIA CO-OP MORTGAGE LENDERS

- CRAWFORDVILLE GEORGIA CO-OP MORTGAGE LENDERS

- CULLODEN GEORGIA CO-OP MORTGAGE LENDERS

- CUMMING GEORGIA CO-OP MORTGAGE LENDERS

- CUSSETA GEORGIA CO-OP MORTGAGE LENDERS

- CUTHBERT GEORGIA CO-OP MORTGAGE LENDERS

- DACULA GEORGIA CO-OP MORTGAGE LENDERS

- DAHLONEGA GEORGIA CO-OP MORTGAGE LENDERS

- DALLAS GEORGIA CO-OP MORTGAGE LENDERS

- DALTON GEORGIA CO-OP MORTGAGE LENDERS

- DAMASCUS GEORGIA CO-OP MORTGAGE LENDERS

- DANIELSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- DANVILLE GEORGIA CO-OP MORTGAGE LENDERS

- DARIEN GEORGIA CO-OP MORTGAGE LENDERS

- DASHER GEORGIA CO-OP MORTGAGE LENDERS

- DAVISBORO GEORGIA CO-OP MORTGAGE LENDERS

- DAWSON GEORGIA CO-OP MORTGAGE LENDERS

- DAWSONVILLE GEORGIA CO-OP MORTGAGE LENDERS

- DE SOTO GEORGIA CO-OP MORTGAGE LENDERS

- DEARING GEORGIA CO-OP MORTGAGE LENDERS

- DECATUR GEORGIA CO-OP MORTGAGE LENDERS

- DEEPSTEP GEORGIA CO-OP MORTGAGE LENDERS

- DEMOREST GEORGIA CO-OP MORTGAGE LENDERS

- DEXTER GEORGIA CO-OP MORTGAGE LENDERS

- DILLARD GEORGIA CO-OP MORTGAGE LENDERS

- DOERUN GEORGIA CO-OP MORTGAGE LENDERS

- DONALSONVILLE GEORGIA CO-OP MORTGAGE LENDERS

- DOOLING GEORGIA CO-OP MORTGAGE LENDERS

- DORAVILLE GEORGIA CO-OP MORTGAGE LENDERS

- DOUGLAS GEORGIA CO-OP MORTGAGE LENDERS

- DOUGLASVILLE GEORGIA CO-OP MORTGAGE LENDERS

- DU PONT GEORGIA CO-OP MORTGAGE LENDERS

- DUBLIN GEORGIA CO-OP MORTGAGE LENDERS

- DUDLEY GEORGIA CO-OP MORTGAGE LENDERS

- DULUTH GEORGIA CO-OP MORTGAGE LENDERS

- DUNWOODY GEORGIA CO-OP MORTGAGE LENDERS

- EAST DUBLIN GEORGIA CO-OP MORTGAGE LENDERS

- EAST ELLIJAY GEORGIA CO-OP MORTGAGE LENDERS

- EAST POINT GEORGIA CO-OP MORTGAGE LENDERS

- EASTMAN GEORGIA CO-OP MORTGAGE LENDERS

- EATONTON GEORGIA CO-OP MORTGAGE LENDERS

- EDGE HILL GEORGIA CO-OP MORTGAGE LENDERS

- EDISON GEORGIA CO-OP MORTGAGE LENDERS

- ELBERTON GEORGIA CO-OP MORTGAGE LENDERS

- ELLAVILLE GEORGIA CO-OP MORTGAGE LENDERS

- ELLENTON GEORGIA CO-OP MORTGAGE LENDERS

- ELLIJAY GEORGIA CO-OP MORTGAGE LENDERS

- EMERSON GEORGIA CO-OP MORTGAGE LENDERS

- ENIGMA GEORGIA CO-OP MORTGAGE LENDERS

- EPHESUS GEORGIA CO-OP MORTGAGE LENDERS

- ETON GEORGIA CO-OP MORTGAGE LENDERS

- EUHARLEE GEORGIA CO-OP MORTGAGE LENDERS

- FAIRBURN GEORGIA CO-OP MORTGAGE LENDERS

- FAIRMOUNT GEORGIA CO-OP MORTGAGE LENDERS

- FARGO GEORGIA CO-OP MORTGAGE LENDERS

- FAYETTEVILLE GEORGIA CO-OP MORTGAGE LENDERS

- FITZGERALD GEORGIA CO-OP MORTGAGE LENDERS

- FLEMINGTON GEORGIA CO-OP MORTGAGE LENDERS

- FLOVILLA GEORGIA CO-OP MORTGAGE LENDERS

- FLOWERY BRANCH GEORGIA CO-OP MORTGAGE LENDERS

- FOLKSTON GEORGIA CO-OP MORTGAGE LENDERS

- FOREST PARK GEORGIA CO-OP MORTGAGE LENDERS

- FORSYTH GEORGIA CO-OP MORTGAGE LENDERS

- FORT GAINES GEORGIA CO-OP MORTGAGE LENDERS

- FORT OGLETHORPE GEORGIA CO-OP MORTGAGE LENDERS

- FORT VALLEY GEORGIA CO-OP MORTGAGE LENDERS

- FRANKLIN GEORGIA CO-OP MORTGAGE LENDERS

- FRANKLIN SPRINGS GEORGIA CO-OP MORTGAGE LENDERS

- FUNSTON GEORGIA CO-OP MORTGAGE LENDERS

- GAINESVILLE GEORGIA CO-OP MORTGAGE LENDERS

- GARDEN CITY GEORGIA CO-OP MORTGAGE LENDERS

- GARFIELD GEORGIA CO-OP MORTGAGE LENDERS

- GAY GEORGIA CO-OP MORTGAGE LENDERS

- GENEVA GEORGIA CO-OP MORTGAGE LENDERS

- GEORGETOWN GEORGIA CO-OP MORTGAGE LENDERS

- GIBSON GEORGIA CO-OP MORTGAGE LENDERS

- GILLSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- GIRARD GEORGIA CO-OP MORTGAGE LENDERS

- GLENNVILLE GEORGIA CO-OP MORTGAGE LENDERS

- GLENWOOD GEORGIA CO-OP MORTGAGE LENDERS

- GOOD HOPE GEORGIA CO-OP MORTGAGE LENDERS

- GORDON GEORGIA CO-OP MORTGAGE LENDERS

- GRAHAM GEORGIA CO-OP MORTGAGE LENDERS

- GRANTVILLE GEORGIA CO-OP MORTGAGE LENDERS

- GRAY GEORGIA CO-OP MORTGAGE LENDERS

- GRAYSON GEORGIA CO-OP MORTGAGE LENDERS

- GREENSBORO GEORGIA CO-OP MORTGAGE LENDERS

- GREENVILLE GEORGIA CO-OP MORTGAGE LENDERS

- GRIFFIN GEORGIA CO-OP MORTGAGE LENDERS

- GROVETOWN GEORGIA CO-OP MORTGAGE LENDERS

- GUMBRANCH GEORGIA CO-OP MORTGAGE LENDERS

- GUYTON GEORGIA CO-OP MORTGAGE LENDERS

- HAGAN GEORGIA CO-OP MORTGAGE LENDERS

- HAHIRA GEORGIA CO-OP MORTGAGE LENDERS

- HAMILTON GEORGIA CO-OP MORTGAGE LENDERS

- HAMPTON GEORGIA CO-OP MORTGAGE LENDERS

- HAPEVILLE GEORGIA CO-OP MORTGAGE LENDERS

- HARALSON GEORGIA CO-OP MORTGAGE LENDERS

- HARLEM GEORGIA CO-OP MORTGAGE LENDERS

- HARRISON GEORGIA CO-OP MORTGAGE LENDERS

- HARTWELL GEORGIA CO-OP MORTGAGE LENDERS

- HAWKINSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- HAZLEHURST GEORGIA CO-OP MORTGAGE LENDERS

- HELEN GEORGIA CO-OP MORTGAGE LENDERS

- HEPHZIBAH GEORGIA CO-OP MORTGAGE LENDERS

- HIAWASSEE GEORGIA CO-OP MORTGAGE LENDERS

- HIGGSTON GEORGIA CO-OP MORTGAGE LENDERS

- HILTONIA GEORGIA CO-OP MORTGAGE LENDERS

- HINESVILLE GEORGIA CO-OP MORTGAGE LENDERS

- HIRAM GEORGIA CO-OP MORTGAGE LENDERS

- HOBOKEN GEORGIA CO-OP MORTGAGE LENDERS

- HOGANSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- HOLLY SPRINGS GEORGIA CO-OP MORTGAGE LENDERS

- HOMELAND GEORGIA CO-OP MORTGAGE LENDERS

- HOMER GEORGIA CO-OP MORTGAGE LENDERS

- HOMERVILLE GEORGIA CO-OP MORTGAGE LENDERS

- HOSCHTON GEORGIA CO-OP MORTGAGE LENDERS

- HULL GEORGIA CO-OP MORTGAGE LENDERS

- IDEAL GEORGIA CO-OP MORTGAGE LENDERS

- ILA GEORGIA CO-OP MORTGAGE LENDERS

- IRON CITY GEORGIA CO-OP MORTGAGE LENDERS

- IRWINTON GEORGIA CO-OP MORTGAGE LENDERS

- IVEY GEORGIA CO-OP MORTGAGE LENDERS

- JACKSON GEORGIA CO-OP MORTGAGE LENDERS

- JACKSONVILLE GEORGIA CO-OP MORTGAGE LENDERS

- JAKIN GEORGIA CO-OP MORTGAGE LENDERS

- JASPER GEORGIA CO-OP MORTGAGE LENDERS

- JEFFERSON GEORGIA CO-OP MORTGAGE LENDERS

- JEFFERSONVILLE GEORGIA CO-OP MORTGAGE LENDERS

- JENKINSBURG GEORGIA CO-OP MORTGAGE LENDERS

- JERSEY GEORGIA CO-OP MORTGAGE LENDERS

- JESUP GEORGIA CO-OP MORTGAGE LENDERS

- JOHNS CREEK GEORGIA CO-OP MORTGAGE LENDERS

- JONESBORO GEORGIA CO-OP MORTGAGE LENDERS

- JUNCTION CITY GEORGIA CO-OP MORTGAGE LENDERS

- KENNESAW GEORGIA CO-OP MORTGAGE LENDERS

- KEYSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- KINGSLAND GEORGIA CO-OP MORTGAGE LENDERS

- KINGSTON GEORGIA CO-OP MORTGAGE LENDERS

- KITE GEORGIA CO-OP MORTGAGE LENDERS

- LAFAYETTE GEORGIA CO-OP MORTGAGE LENDERS

- LAGRANGE GEORGIA CO-OP MORTGAGE LENDERS

- LAKE CITY GEORGIA CO-OP MORTGAGE LENDERS

- LAKE PARK GEORGIA CO-OP MORTGAGE LENDERS

- LAKELAND GEORGIA CO-OP MORTGAGE LENDERS

- LAVONIA GEORGIA CO-OP MORTGAGE LENDERS

- LAWRENCEVILLE GEORGIA CO-OP MORTGAGE LENDERS

- LEARY GEORGIA CO-OP MORTGAGE LENDERS

- LEESBURG GEORGIA CO-OP MORTGAGE LENDERS

- LENOX GEORGIA CO-OP MORTGAGE LENDERS

- LESLIE GEORGIA CO-OP MORTGAGE LENDERS

- LEXINGTON GEORGIA CO-OP MORTGAGE LENDERS

- LILBURN GEORGIA CO-OP MORTGAGE LENDERS

- LILLY GEORGIA CO-OP MORTGAGE LENDERS

- LINCOLNTON GEORGIA CO-OP MORTGAGE LENDERS

- LITHONIA GEORGIA CO-OP MORTGAGE LENDERS

- LOCUST GROVE GEORGIA CO-OP MORTGAGE LENDERS

- LOGANVILLE GEORGIA CO-OP MORTGAGE LENDERS

- LONE OAK GEORGIA CO-OP MORTGAGE LENDERS

- LOOKOUT MOUNTAIN GEORGIA CO-OP MORTGAGE LENDERS

- LOUISVILLE GEORGIA CO-OP MORTGAGE LENDERS

- LOVEJOY GEORGIA CO-OP MORTGAGE LENDERS

- LUDOWICI GEORGIA CO-OP MORTGAGE LENDERS

- LULA GEORGIA CO-OP MORTGAGE LENDERS

- LUMBER CITY GEORGIA CO-OP MORTGAGE LENDERS

- LUMPKIN GEORGIA CO-OP MORTGAGE LENDERS

- LUTHERSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- LYERLY GEORGIA CO-OP MORTGAGE LENDERS

- LYONS GEORGIA CO-OP MORTGAGE LENDERS

- MACON GEORGIA CO-OP MORTGAGE LENDERS

- MADISON GEORGIA CO-OP MORTGAGE LENDERS

- MANASSAS GEORGIA CO-OP MORTGAGE LENDERS

- MANCHESTER GEORGIA CO-OP MORTGAGE LENDERS

- MANSFIELD GEORGIA CO-OP MORTGAGE LENDERS

- MARIETTA GEORGIA CO-OP MORTGAGE LENDERS

- MARSHALLVILLE GEORGIA CO-OP MORTGAGE LENDERS

- MARTIN GEORGIA CO-OP MORTGAGE LENDERS

- MAXEYS GEORGIA CO-OP MORTGAGE LENDERS

- MAYSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- MCCAYSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- MCDONOUGH GEORGIA CO-OP MORTGAGE LENDERS

- MCINTYRE GEORGIA CO-OP MORTGAGE LENDERS

- MCRAE-HELENA GEORGIA CO-OP MORTGAGE LENDERS

- MEANSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- MEIGS GEORGIA CO-OP MORTGAGE LENDERS

- MENLO GEORGIA CO-OP MORTGAGE LENDERS

- METTER GEORGIA CO-OP MORTGAGE LENDERS

- MIDVILLE GEORGIA CO-OP MORTGAGE LENDERS

- MIDWAY GEORGIA CO-OP MORTGAGE LENDERS

- MILAN GEORGIA CO-OP MORTGAGE LENDERS

- MILLEDGEVILLE GEORGIA CO-OP MORTGAGE LENDERS

- MILLEN GEORGIA CO-OP MORTGAGE LENDERS

- MILNER GEORGIA CO-OP MORTGAGE LENDERS

- MILTON GEORGIA CO-OP MORTGAGE LENDERS

- MITCHELL GEORGIA CO-OP MORTGAGE LENDERS

- MOLENA GEORGIA CO-OP MORTGAGE LENDERS

- MONROE GEORGIA CO-OP MORTGAGE LENDERS

- MONTEZUMA GEORGIA CO-OP MORTGAGE LENDERS

- MONTICELLO GEORGIA CO-OP MORTGAGE LENDERS

- MONTROSE GEORGIA CO-OP MORTGAGE LENDERS

- MORELAND GEORGIA CO-OP MORTGAGE LENDERS

- MORGAN GEORGIA CO-OP MORTGAGE LENDERS

- MORGANTON GEORGIA CO-OP MORTGAGE LENDERS

- MORROW GEORGIA CO-OP MORTGAGE LENDERS

- MORVEN GEORGIA CO-OP MORTGAGE LENDERS

- MOULTRIE GEORGIA CO-OP MORTGAGE LENDERS

- MOUNT AIRY GEORGIA CO-OP MORTGAGE LENDERS

- MOUNT VERNON GEORGIA CO-OP MORTGAGE LENDERS

- MOUNT ZION GEORGIA CO-OP MORTGAGE LENDERS

- MOUNTAIN CITY GEORGIA CO-OP MORTGAGE LENDERS

- MOUNTAIN PARK GEORGIA CO-OP MORTGAGE LENDERS

- NAHUNTA GEORGIA CO-OP MORTGAGE LENDERS

- NASHVILLE GEORGIA CO-OP MORTGAGE LENDERS

- NELSON GEORGIA CO-OP MORTGAGE LENDERS

- NEWBORN GEORGIA CO-OP MORTGAGE LENDERS

- NEWINGTON GEORGIA CO-OP MORTGAGE LENDERS

- NEWNAN GEORGIA CO-OP MORTGAGE LENDERS

- NEWTON GEORGIA CO-OP MORTGAGE LENDERS

- NICHOLLS GEORGIA CO-OP MORTGAGE LENDERS

- NICHOLSON GEORGIA CO-OP MORTGAGE LENDERS

- NORCROSS GEORGIA CO-OP MORTGAGE LENDERS

- NORMAN PARK GEORGIA CO-OP MORTGAGE LENDERS

- NORTH HIGH SHOALS GEORGIA CO-OP MORTGAGE LENDERS

- NORWOOD GEORGIA CO-OP MORTGAGE LENDERS

- OAK PARK GEORGIA CO-OP MORTGAGE LENDERS

- OAKWOOD GEORGIA CO-OP MORTGAGE LENDERS

- OCHLOCKNEE GEORGIA CO-OP MORTGAGE LENDERS

- OCILLA GEORGIA CO-OP MORTGAGE LENDERS

- OCONEE GEORGIA CO-OP MORTGAGE LENDERS

- ODUM GEORGIA CO-OP MORTGAGE LENDERS

- OFFERMAN GEORGIA CO-OP MORTGAGE LENDERS

- OGLETHORPE GEORGIA CO-OP MORTGAGE LENDERS

- OLIVER GEORGIA CO-OP MORTGAGE LENDERS

- OMEGA GEORGIA CO-OP MORTGAGE LENDERS

- ORCHARD HILL GEORGIA CO-OP MORTGAGE LENDERS

- OXFORD GEORGIA CO-OP MORTGAGE LENDERS

- PALMETTO GEORGIA CO-OP MORTGAGE LENDERS

- PARROTT GEORGIA CO-OP MORTGAGE LENDERS

- PATTERSON GEORGIA CO-OP MORTGAGE LENDERS

- PAVO GEORGIA CO-OP MORTGAGE LENDERS

- PAYNE CITY GEORGIA CO-OP MORTGAGE LENDERS

- PEACHTREE CITY GEORGIA CO-OP MORTGAGE LENDERS

- PEACHTREE CORNERS GEORGIA CO-OP MORTGAGE LENDERS

- PEARSON GEORGIA CO-OP MORTGAGE LENDERS

- PELHAM GEORGIA CO-OP MORTGAGE LENDERS

- PEMBROKE GEORGIA CO-OP MORTGAGE LENDERS

- PENDERGRASS GEORGIA CO-OP MORTGAGE LENDERS

- PERRY GEORGIA CO-OP MORTGAGE LENDERS

- PINE LAKE GEORGIA CO-OP MORTGAGE LENDERS

- PINE MOUNTAIN GEORGIA CO-OP MORTGAGE LENDERS

- PINEHURST GEORGIA CO-OP MORTGAGE LENDERS

- PINEVIEW GEORGIA CO-OP MORTGAGE LENDERS

- PITTS GEORGIA CO-OP MORTGAGE LENDERS

- PLAINS GEORGIA CO-OP MORTGAGE LENDERS

- PLAINVILLE GEORGIA CO-OP MORTGAGE LENDERS

- POOLER GEORGIA CO-OP MORTGAGE LENDERS

- PORT WENTWORTH GEORGIA CO-OP MORTGAGE LENDERS

- PORTAL GEORGIA CO-OP MORTGAGE LENDERS

- PORTERDALE GEORGIA CO-OP MORTGAGE LENDERS

- POULAN GEORGIA CO-OP MORTGAGE LENDERS

- POWDER SPRINGS GEORGIA CO-OP MORTGAGE LENDERS

- PRESTON GEORGIA CO-OP MORTGAGE LENDERS

- PULASKI GEORGIA CO-OP MORTGAGE LENDERS

- QUITMAN GEORGIA CO-OP MORTGAGE LENDERS

- RANGER GEORGIA CO-OP MORTGAGE LENDERS

- RAY CITY GEORGIA CO-OP MORTGAGE LENDERS

- RAYLE GEORGIA CO-OP MORTGAGE LENDERS

- REBECCA GEORGIA CO-OP MORTGAGE LENDERS

- REGISTER GEORGIA CO-OP MORTGAGE LENDERS

- REIDSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- REMERTON GEORGIA CO-OP MORTGAGE LENDERS

- RENTZ GEORGIA CO-OP MORTGAGE LENDERS

- RESACA GEORGIA CO-OP MORTGAGE LENDERS

- REYNOLDS GEORGIA CO-OP MORTGAGE LENDERS

- RHINE GEORGIA CO-OP MORTGAGE LENDERS

- RICEBORO GEORGIA CO-OP MORTGAGE LENDERS

- RICHLAND GEORGIA CO-OP MORTGAGE LENDERS

- RICHMOND HILL GEORGIA CO-OP MORTGAGE LENDERS

- RIDDLEVILLE GEORGIA CO-OP MORTGAGE LENDERS

- RINCON GEORGIA CO-OP MORTGAGE LENDERS

- RINGGOLD GEORGIA CO-OP MORTGAGE LENDERS

- RIVERDALE GEORGIA CO-OP MORTGAGE LENDERS

- RIVERSIDE GEORGIA CO-OP MORTGAGE LENDERS

- ROBERTA GEORGIA CO-OP MORTGAGE LENDERS

- ROCHELLE GEORGIA CO-OP MORTGAGE LENDERS

- ROCKMART GEORGIA CO-OP MORTGAGE LENDERS

- ROCKY FORD GEORGIA CO-OP MORTGAGE LENDERS

- ROME GEORGIA CO-OP MORTGAGE LENDERS

- ROSSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- ROSWELL GEORGIA CO-OP MORTGAGE LENDERS

- ROYSTON GEORGIA CO-OP MORTGAGE LENDERS

- RUTLEDGE GEORGIA CO-OP MORTGAGE LENDERS

- SALE CITY GEORGIA CO-OP MORTGAGE LENDERS

- SANDERSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- SANDY SPRINGS GEORGIA CO-OP MORTGAGE LENDERS

- SANTA CLAUS GEORGIA CO-OP MORTGAGE LENDERS

- SARDIS GEORGIA CO-OP MORTGAGE LENDERS

- SASSER GEORGIA CO-OP MORTGAGE LENDERS

- SAVANNAH GEORGIA CO-OP MORTGAGE LENDERS

- SCOTLAND GEORGIA CO-OP MORTGAGE LENDERS

- SCREVEN GEORGIA CO-OP MORTGAGE LENDERS

- SENOIA GEORGIA CO-OP MORTGAGE LENDERS

- SHADY DALE GEORGIA CO-OP MORTGAGE LENDERS

- SHARON GEORGIA CO-OP MORTGAGE LENDERS

- SHARPSBURG GEORGIA CO-OP MORTGAGE LENDERS

- SHELLMAN GEORGIA CO-OP MORTGAGE LENDERS

- SHILOH GEORGIA CO-OP MORTGAGE LENDERS

- SILOAM GEORGIA CO-OP MORTGAGE LENDERS

- SKY VALLEY GEORGIA CO-OP MORTGAGE LENDERS

- SMITHVILLE GEORGIA CO-OP MORTGAGE LENDERS

- SMYRNA GEORGIA CO-OP MORTGAGE LENDERS

- SNELLVILLE GEORGIA CO-OP MORTGAGE LENDERS

- SOCIAL CIRCLE GEORGIA CO-OP MORTGAGE LENDERS

- SOPERTON GEORGIA CO-OP MORTGAGE LENDERS

- SPARKS GEORGIA CO-OP MORTGAGE LENDERS

- SPARTA GEORGIA CO-OP MORTGAGE LENDERS

- SPRINGFIELD GEORGIA CO-OP MORTGAGE LENDERS

- ST. MARYS GEORGIA CO-OP MORTGAGE LENDERS

- STAPLETON GEORGIA CO-OP MORTGAGE LENDERS

- STATENVILLE GEORGIA CO-OP MORTGAGE LENDERS

- STATESBORO GEORGIA CO-OP MORTGAGE LENDERS

- STATHAM GEORGIA CO-OP MORTGAGE LENDERS

- STILLMORE GEORGIA CO-OP MORTGAGE LENDERS

- STOCKBRIDGE GEORGIA CO-OP MORTGAGE LENDERS

- STONE MOUNTAIN GEORGIA CO-OP MORTGAGE LENDERS

- SUGAR HILL GEORGIA CO-OP MORTGAGE LENDERS

- SUMMERVILLE GEORGIA CO-OP MORTGAGE LENDERS

- SUMNER GEORGIA CO-OP MORTGAGE LENDERS

- SURRENCY GEORGIA CO-OP MORTGAGE LENDERS

- SUWANEE GEORGIA CO-OP MORTGAGE LENDERS

- SWAINSBORO GEORGIA CO-OP MORTGAGE LENDERS

- SYCAMORE GEORGIA CO-OP MORTGAGE LENDERS

- SYLVANIA GEORGIA CO-OP MORTGAGE LENDERS

- SYLVESTER GEORGIA CO-OP MORTGAGE LENDERS

- TALBOTTON GEORGIA CO-OP MORTGAGE LENDERS

- TALKING ROCK GEORGIA CO-OP MORTGAGE LENDERS

- TALLAPOOSA GEORGIA CO-OP MORTGAGE LENDERS

- TALLULAH FALLS GEORGIA CO-OP MORTGAGE LENDERS

- TALMO GEORGIA CO-OP MORTGAGE LENDERS

- TARRYTOWN GEORGIA CO-OP MORTGAGE LENDERS

- TAYLORSVILLE GEORGIA CO-OP MORTGAGE LENDERS

- TEMPLE GEORGIA CO-OP MORTGAGE LENDERS

- TENNILLE GEORGIA CO-OP MORTGAGE LENDERS

- THOMASTON GEORGIA CO-OP MORTGAGE LENDERS

- THOMASVILLE GEORGIA CO-OP MORTGAGE LENDERS

- THOMSON GEORGIA CO-OP MORTGAGE LENDERS

- THUNDERBOLT GEORGIA CO-OP MORTGAGE LENDERS

- TIFTON GEORGIA CO-OP MORTGAGE LENDERS

- TIGNALL GEORGIA CO-OP MORTGAGE LENDERS

- TOCCOA GEORGIA CO-OP MORTGAGE LENDERS

- TOOMSBORO GEORGIA CO-OP MORTGAGE LENDERS

- TRENTON GEORGIA CO-OP MORTGAGE LENDERS

- TRION GEORGIA CO-OP MORTGAGE LENDERS

- TUNNEL HILL GEORGIA CO-OP MORTGAGE LENDERS

- TURIN GEORGIA CO-OP MORTGAGE LENDERS

- TWIN CITY GEORGIA CO-OP MORTGAGE LENDERS

- TY TY GEORGIA CO-OP MORTGAGE LENDERS

- TYBEE ISLAND GEORGIA CO-OP MORTGAGE LENDERS

- TYRONE GEORGIA CO-OP MORTGAGE LENDERS

- UNADILLA GEORGIA CO-OP MORTGAGE LENDERS

- UNION CITY GEORGIA CO-OP MORTGAGE LENDERS

- UNION POINT GEORGIA CO-OP MORTGAGE LENDERS

- UVALDA GEORGIA CO-OP MORTGAGE LENDERS

- VALDOSTA GEORGIA CO-OP MORTGAGE LENDERS

- VARNELL GEORGIA CO-OP MORTGAGE LENDERS

- VERNONBURG GEORGIA CO-OP MORTGAGE LENDERS

- VIDALIA GEORGIA CO-OP MORTGAGE LENDERS

- VIENNA GEORGIA CO-OP MORTGAGE LENDERS

- VILLA RICA GEORGIA CO-OP MORTGAGE LENDERS